The Laffer Curve and Supply-Side Economics

The Laffer curve is the centerpiece of so-called supply-side economics. The idea behind both concepts is straightforward. Here it is, in my words:

Taxes inhibit economic activity, especially because progressive tax rates reduce saving among persons with higher incomes and, thereby, reduce the flow of funds available for growth-producing capital investments (e.g., new manufacturing equipment, better computers, R&D on drugs that improve the health of workers and others). Lower tax rates therefore foster a higher rate of economic growth. The economic growth that is fostered by tax-rate reductions may, in some instances, cause tax revenues to rise.

Many commentators accept that reductions in tax rates spur economic growth. Far fewer accept that faster economic growth will, in turn, cause tax revenues to rise. (For various views on the matter, see this, this, this, this, this, and this.)

Questions and Brief Answers

The Laffer hypothesis, and criticisms of it, stir me to ask (and answer) these questions:

- Would tax rates below (above) the current level spur (inhibit) economic growth?

- If so, by how much?

- At what tax rate would revenues be maximized?

- Are tax revenues more important than economic growth?

My brief answers are these:

- Yes, changes in tax rates cause economic growth to move in the opposite direction.

- By a lot.

- It is possible to estimate the rate at which tax revenues are maximized, but who would want to maximize them, other than a “fiscally responsible” (i.e., tax-and-spend) “liberal”?

- Only to a tax-and-spend “liberal.”

In what follows, I enlarge on those answers.

The Laffer Curve, in Theory

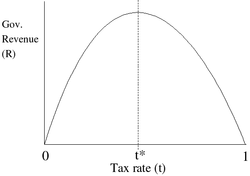

I begin with this depiction of the Laffer curve (via Wikipedia):

t* represents the rate of taxation at which maximal revenue is generated. Note: This diagram is not to scale; t* could theoretically be anywhere, not necessarily in the vicinity of 50% as shown here.

Many criticisms of the Laffer curve are recited here (not all of which I accept). My main reservation about the curve is its span:

- With real taxes (i.e., government spending) at zero or close to it, the rule of law would break down and the economy would collapse. Thus the curve should not extend to zero on the x-axis.

- With real taxes (i.e., government spending) at very high rates (much about the level of 50 percent, which the U.S. reached in World War II), the economy would be subsumed by government.

The Proper Range of the Laffer Curve

With regard to the first problem, I would set the minimum tax rate at 15 percent of GDP. The normal peacetime burden of government spending between the end of the Civil War and the eve of the Great Depression ranged from 5 to 10 percent of GDP,1 enough to maintain law and order and to provide minimal “social services.” To that I would add 5 to 10 percent for the kind of defense that we need in these parlous times. (See this post, for example.)

I therefore consider a tax rate of 15 percent to be the lowest rate of interest along the x-axis of the Laffer curve. I include in that 15-percent rate taxes levied by all levels of government, not only to to fund governmental functions (e.g., justice and defense) but also to fund social transfers (e.g., Social Security).

As for the second problem, at a very high tax rate we would have a command economy (as in the former Soviet Union). At a tax rate of 100 percent, for example, government would have to confiscate everyone’s income, then turn around and refund that income to everyone in the form of government-dictated access to goods and services. Those goods and services would, of necessity, be produced by the populace at the direction of government; there would be no private sector.2 Everyone — excepting brave black-marketeers — would be a government employee or contractor. The distribution of income in a Soviet-style economy does not, of course, match the distribution of income in a market economy. A Soviet-style economy, rather, operates on the following principle: “From each according to his ability, to each — especially the commissariat and its favorites — according to his needs.”

The U.S. economy was practically a command economy during World War II, when government commandeered as much as 50 percent of the nation’s output. (See the graph in the footnote to this post.) I therefore regard 50 percent as the highest meaningful value along the x-axis of the Laffer curve.

Quantifying the Laffer Curve and More Important Values

In sum, the Laffer curve is relevant over the range of a 15-percent to 50-percent tax rate. And the Laffer curve can be quantified over that range. To quantify it, I draw on “The Macroeconomic Effects of Tax Changes: Estimates Based on a New Measure of Fiscal Shocks,” by Christina D. Romer and David H. Romer, both of the Department of Economics at the University of California, Berkeley. (A free copy of the paper is available here. A copy is available here for $5.)

The Romers’ estimate, among other things, the effects of exogenous changes in taxes on GDP. (“Exogenous” meaning tax cuts aimed at stimulating the economy, as opposed — for example — to tax increases aimed at reducing government deficits.) Here is the key finding, from pages 21 and 22 of the free version of the paper:

Figure 4 summarizes the estimates by showing the implied effect of a tax increase of one percent of GDP on the path of real GDP (in logarithms), together with the one-standard-error bands. The effect is steadily down, first slowly and then more rapidly, finally leveling off after ten quarters. The estimated maximum impact is a fall in output of 3.0 percent. This estimate is overwhelmingly significant (t = 3.5). The two-standard-error confidence interval is (4.7%,1.3%). In short, tax increases appear to have a very large, sustained, and highly significant negative impact on output. Since most of our exogenous tax changes are in fact reductions, the more intuitive way to express this result is that tax cuts have very large and persistent positive output effects.

The Romers assess the effects of tax cuts over a period of only 12 quarters (3 years). Some of the resulting growth in GDP during that period takes the form of greater spending on capital investments, the payoff from which usually takes more than 3 years to realize. So, a 1-percent tax cut yields more than a 3-percent rise in GDP, over the longer run. How much more? About 0.25 percent. Thus a tax cut of 1 percent of GDP yields a total, long-run increase in GDP of about 3.25 percent.3

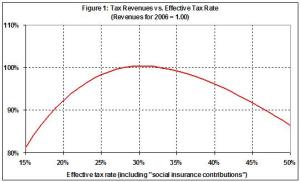

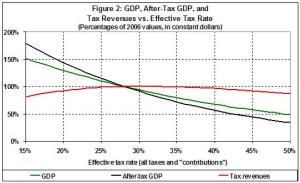

With that number in hand, and knowing the current, effective tax rate (28 percent of GDP in 20064), it is then easy to compute GDP, tax revenues, and after-tax GDP as a function of the overall tax rate. The following graphs display those values in index form, where 1.00 is the value in 2006. Figure 1 is my estimate of the Laffer curve. Figure 2 contrasts the Laffer curve with more important values, namely, the effects of tax-rate changes on GDP and after-tax GDP.

Questions and Answers, Revisited

I return now to the earlier questions, and expand on my brief answers to them:

- Q. Would tax rates below/above the current level spur/inhibit economic growth? A. Yes, lower tax rates would spur growth and higher tax rates would inhibit growth — markedly, in both cases.

- Q. If so, by how much? A. Reducing taxes to an effective rate of 15 percent of GDP, for example, would lead to an increase in GDP of about 50 percent and an increase in after-tax GDP of about 80 percent. An effective tax rate of 40 percent, on the other hand, would lead to a one-third decrease in GDP and a 45-percent decrease in after-tax GDP.

- Q. At what tax rate would revenues be maximized? A. An increase in the effective tax rate from 28 percent to 30 percent would cause tax revenues to rise by 0.3 percent (that’s three-tenths of 1 percent). Wow! As a result of that “fiscally responsible” increase, GDP would drop by 6 percent and after-tax GDP would drop by 9 percent.

- Q. Are tax revenues more important than economic growth? A. No. Why? First, see the answer to question number 3. Then, consider this: It is blind stupidity to focus on tax revenues. The economy does not exist for the purpose of generating tax revenues, it exists for the purpose of providing goods and services for today’s use and “wealth” (in such forms as housing and savings) for use over the longer term (e.g., for our children’s education and our retirement). It is necessary to divert a minimal fraction of economic output to government (about 15 percent, nowadays), for the purpose of protecting ourselves and our economic activities from predators, foreign and domestic. Any diversion beyond that is pure waste.

The Laffer Curve Puts the Emphasis on the Wrong Economic Variable

I cannot over-emphasize this point: The Laffer curve does a great disservice by emphasizing tax revenues, when the proper emphasis is on economic growth. Government doesn’t create jobs; on balance, it only destroys them, through taxation (and regulation).

By focusing on tax revenues, Lafferites play into the hands of “fiscally responsible” (i.e., tax-and-spend) “liberals” (i.e. Leftists). The Left is interested in neither fiscal responsibility nor economic growth. The Left simply wants to raise taxes in order to pay for more social goodies, and that’s that. In return for those goodies, most of us — even including the Left’s protégés — would get less of everything. The proof of that statement is found not only in the Romers’ analysis, but also in the case study of economic suicide that is Michigan, and in the retrogressive economic history of the United States.

Yet, the Left (i.e., Charlie Rangel and friends) want to pay for their social goodies by levying punitive taxes on the so-called “super-rich” — those high-earning, highly productive citizens who, on the one hand, finance economic growth and, on the other hand, implement it through hard work, entrepreneurship, and innovativeness. They already subsidize the rest of us when it comes to taxes (e.g., here, here, here, here, and here). Forcing the “rich” to pay more will only cause economic harm to the rest of us.

(UPDATE, 10/31/07: It is good news that the tax-rate cuts in 2003 seem to have yielded higher tax revenues, because the apparent correlation between lower tax rates and higher revenues seems to confirm the Laffer effect. It is bad news that tax revenues have risen, because the money would have been used more productively in the private sector. My take, however, is that tax revenues have risen mainly because of cyclical growth. I don’t doubt the stimulus afforded by tax-rate cuts; I simply doubt the presence of a Laffer effect at the effective tax rate in 2003, which was 26 percent.

This, on the other hand is good news: lower taxes for the highest earners. The highest earners save and invest more than the rest of us. And that means more economic growth for all of us.

If you’re super-duper rich — as is Warren Buffet — and you think your taxes are too low, take this advice: Voluntarily write a check to the Treasury, and shut up. But don’t propound a rise in marginal tax rates at the high end of the income distribution.)

Coda

So, Mr. Laffer is entirely correct when he writes:

Lower tax rates change people’s economic behavior and stimulate economic growth….

Unfortunately, instead of stopping there, he adds:

…which can create more–not less–tax revenues.

Tax-rate reductions (down to about 15 percent of GDP) will always stimulate economic growth, but they will not always result in higher tax revenues. The mistake that Mr. Laffer and his followers make is to argue that tax cuts lead inexorably to higher tax revenues. In doing so, they play into the hands of tax-and-spend Leftists.

Growth, growth, growth! That’s the winning mantra.

__________

1. See “Martin’s estimates” in Series F216-225, “Percent Distribution of National Income or Aggregate Payments, by Industry, in Current Prices: 1869-1968,” in Chapter F, National Income and Wealth, Historical Statistics of the United States, Colonial Times to 1970: Part 1.

2. Aggregate income (the claims on or distribution of output) must be equal to the aggregate of all types of output.Income and output (the two faces of GDP) in a closed economy (no imports or exports) can be expressed in terms of certain parameters:

Income = C + S + T

Output = C + I + G,

where the parameters are defined as follows:

C = consumption (private-sector consumption of goods and services produced domestically, excluding consumption that is subsidized by government transfer payments to the beneficiaries of such programs Social Security and Medicare)

S = saving (private-sector income not consumed, taxed, or spent on imports)

I = private-sector investment (output invested by non-governmental entities in technology, buildings, equipment, etc., for the purpose of increasing the future output of goods and services)

T = taxes, including transfer-payment taxes for Social Security, etc.

G = government spending (including spending that is subsidized by transfer payments for such programs as Social Security and Medicare)

(These definitions vary from the standard version in that any spending subsidized by government transfer payments for such programs as Social Security and Medicare is included in G rather than C . These definitions also implicitly reject a role for government in saving and investment, for reasons spelled out in my post, “Joe Stiglitz, Ig-Nobelist.”)

It is trivial to show that as government commandeers all output (G = GDP), the values for C and I must shrink to zero.

But, since C (if not I) cannot be reduced to zero without starving the populace and thus reducing its output to zero, government must allocate some G to C. That which it does not allocate to C or fritter away in entirely wasteful endeavors becomes S (and therefore I), by default. But under such a regime, C, S, and I become entirely different — quantitatively and qualitatively — than they would be under a quasi-free-market regime, such as we have in the United States.

Related posts:

Why Government Spending Is Inherently Inflationary

Trade, Government Spending, and Economic Growth

3. Figure 14.c on page 70 of the free version of the Romers’ paper indicates that a 1-percent tax cut leads to a rise in fixed, nonresidential (i.e., business) investment of about 6 percent. Given that business investment is about one-tenth of GDP (see table 3, here), business investment accounts for about 1.8 percentage points of a 3 percentage point rise in GDP (6 x 1/10 x 3 = 1.8).

More importantly, that 1.8-percent rise in investment spending yields, over the longer run, something like an additional 0.25-percent growth in GDP, assuming a rate of return on business investment (capital) of 10-15 percent. See, for example, the bottom panel of figure 3 in “Growth, Productivity, and the Rate of Return on Capital,” by Charles Adams and Bankim Chadha. (For more about investment and its economic effects, see this tutorial.)

Additional growth of 0.25 percent a year might seem like small change, but over 25 years it adds 5 percent to GDP. That’s $660 billion in 2006 dollars — more than $200 per capita.

4. Taxes collected by all levels of government in the U.S. in 2006 (including “social insurance contributions”) amounted to $3,697 billion. GDP in 2006 was $13,195 billion. (These estimates are from the U.S. Department of Commerce, Bureau of Economic Analysis, National Income and Product Accounts, tables 1.1.5 and 3.1, respectively.) Thus the effective tax rate in 2006 was 28.0 percent.

{kind=link}