A recent post, “Government in Macroeconomic Perspective,” is dauntingly long and replete with equations. The equations are simple ones, but may be off-putting to readers who are allergic to mathematical notation. Herewith is an abridged version of the post. Please refer to the original for details of the argument and references to supporting material.

A nation’s aggregate economic activity usually is measured by its Gross Domestic Product (GDP). I accept GDP as an aggregate, monetary measure of national output. But it is impossible to sum the true value of the myriad economic transactions that GDP is supposed to represent because each transaction means something different to the participants in the transaction; that is, the true value of economic goods is subjective.

GDP, nevertheless, affords a rough measure of the general level of a nation’s material output, that is, the rate at which goods and services are being produced (exclusive of such important things as “household production”). All things being the same, a large fraction of a nation’s citizens — but certainly not all of them — will be better off materially if GDP is growing and worse off if it is shrinking. Governmental activities have led to an economy that produces a small fraction of its potential output. And yet, the true believers in big government seek to make it larger and ever more destructive.

Government spending – beyond a certain level — does not increase GDP, but generally redistributes and decreases it. Government spending is beneficial up to the point where it becomes a drain on GDP; that is, at the point where government exceeds a minimal, protective role and acts in ways that discourage productive effort.

Government spending enables governmental activities of five types:

- transfer payments to individuals (e.g., Social Security), which impose costs because the payments transfer income to those who did not earn from those who did;

- de facto transfer payments, namely, the compensation of government employees, and the compensation that flows to the employees, shareholders, and creditors of government contractors – all of which must be financed by private-sector entitites;

- purchases of consumables and capital that are used directly by government in the provision of government services (e.g., fuel for government vehicles, electricity for government buildings, government vehicles, and government buildings);

- the continuation, initiation, modification, and enforcement of tax codes, regulations, administrative procedures, statutes, ordinances, executive orders, and judicial decrees; and

- the financing of items 1 – 4.

The net effect of items 1 and 2 is almost certainly a reduction of GDP. Why? The diversion of income to the unproductive (e.g., persons on Social Security) and counterproductive (e.g., government employees who write and enforce regulations) – by whatever means (taxing or borrowing) is bound to disincentivize work, saving, innovation, and investment. That causes GDP to be lower than it otherwise would be, but the effect is multiplicative, not merely a matter of addition or subtraction. (A Keynesian would argue that the actions encompassed in item 1 tend to raise GDP because the recipients of nominal transfer payments probably have higher marginal propensities to consume than do the persons from whom the transfer payments are exacted. This facile claim overlooks the disincentivizing effects of taxation on the more productive components of an economy, and on the resulting reduction in work effort and growth-producing investment.)

Similarly, the diversion of resources to items 3 and 4 cannot be thought of as additions to or subtractions from GDP, but as multiplicative, because of the same kind of disincentivizing leverage. For example, one effect of item 4 is the unobserved but very real burden placed on the private sector by federal regulations. It has been estimated, reliably, that those regulations impose a hidden cost greater than 15 percent of GDP.

Then there is item 5: financing. In the end, it matters not whether governmental activities are financed by borrowing or taxation, and if by borrowing, whether the lenders are domestic or foreign. This is because it is government spending that diverts resources from private uses, and it is government spending that enables destructive governmental activities (e.g., the writing and enforcement of regulations).

Government long ago became larger than necessary to perform its minimal protective functions. Consider what has happened since 1890, when the early legislative “accomplishments” of the Progressive Era – the establishment of the Interstate Commerce Commission in 1887 and the passage of the Sherman Antitrust Act in 1890 – began to weigh on the economy.

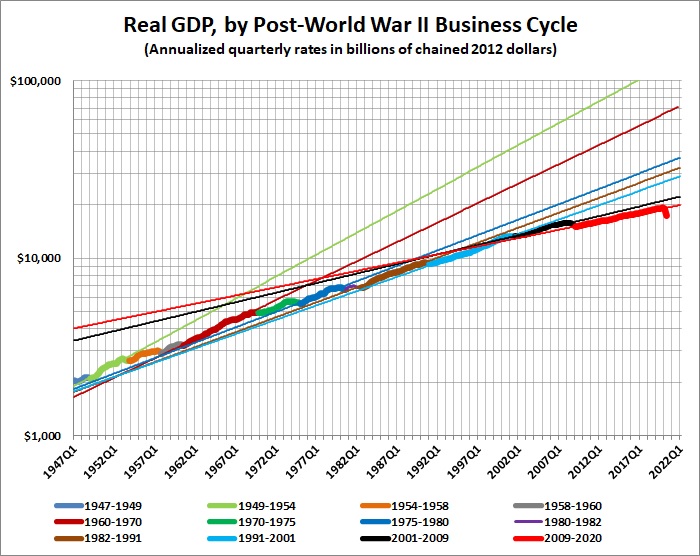

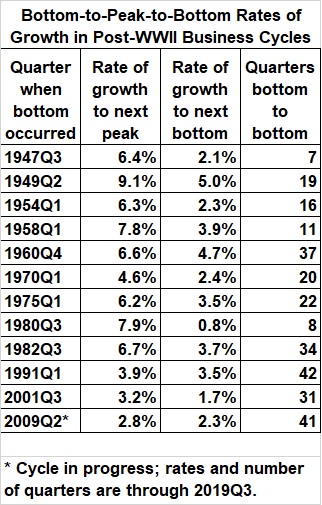

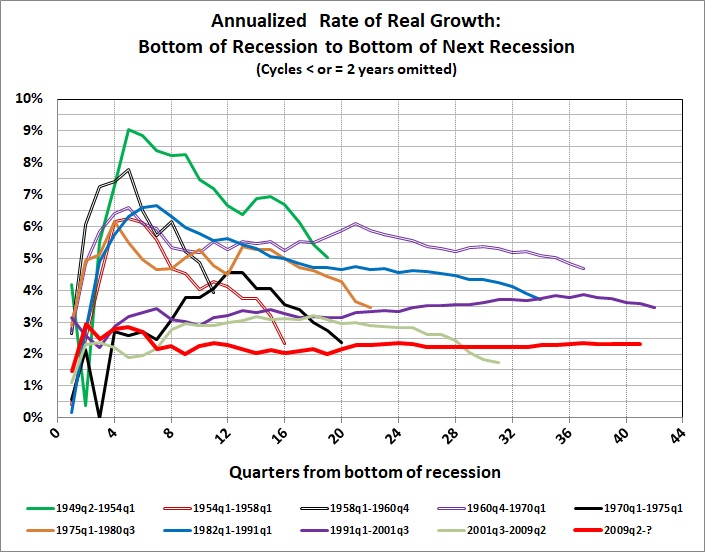

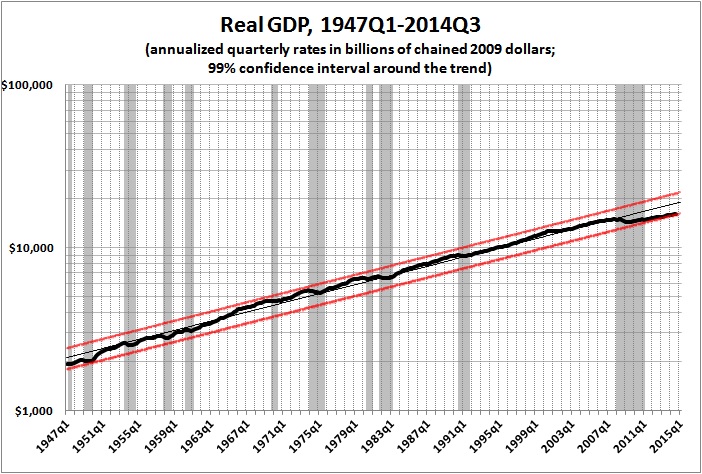

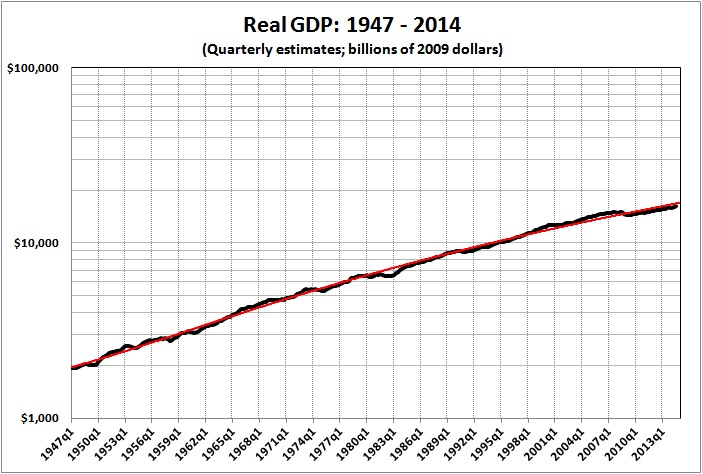

Real GDP (in year 2005 dollars) was $319 billion in 1890; it had risen to $13.3 trillion in 2011 — a compound growth rate of about 3.1 percent. But real GDP in 2011 would have been more than $104 trillion had growth continued at an annual rate of 4.9 percent after 1890 (the rate of growth from 1866 through 1890). What happened? The heavy hand of government (at all levels) — especially after 1929 — made itself felt by discouraging work, discouraging the saving that makes investment possible, discouraging innovation, and (even to the extent that innovation persists) discouraging the investments required to bring innovation on line. How? It begins with the diversion of resources to governmental activities, and is compounded by the cumulative disincentivizing effects of taxes, regulations, administrative procedures, statutes, ordinances, executive orders, and judicial decrees.

Defenders of big government will say that the rate of growth could not have been sustained at something like 5 percent. But such an assertion, if it is based on anything other than ignorance, is based on a simple, sub-exponential model of growth, where returns on investment are diminishing. This model overlooks the effects of innovation and recombination (the use of previous innovations in new ways). If the model of ever-diminishing growth were correct, the U.S. economy would not have experienced rising growth in the first 20 to 25 years after the end of World War II. No, the defenders of sub-exponential growth must look to the Great Society — and to the continuous expansion of the regulatory-welfare state — if they wish to understand the artificially low rate at which the economy is growing: currently about 2 percent a year.

Despite what I have said here about the deleterious effects of bigger-than-minimal government, there are true believers who maintain that the greater the scope and scale of government, the better and richer America will be. These true believers evidently have not considered the cumulative effect of big government on the incomes and wealth of Americans. As the preceding analysis suggests, those relatively few Americans who would not be better off with minimal government would be the beneficiaries of a pool of charitable giving that is vastly greater than the present pool.

That big government might be harmful, even to the “little people” who are its supposed beneficiaries, is of no account to its worshipers – as long as they run it, advise in the running of it, profit by it, or simply enjoy watching it run roughshod over the lives and fortunes of others. Power and the vicarious enjoyment of power are habit-forming drugs.

The ranks of true believers are peopled such left-wing economists as Brad DeLong, James K. Galbraith, and Paul Krugman. They adhere to and popularize two major rationalizations of big government — the Keynesian fallacy and the myth that government is the same as community.

In “A Keynesian Fantasy Land” I discuss six reasons for the ineffectiveness of Keynesian “stimulus”; in summary:

1. The “leakage” to imports

“Part of the extra spending stimulus fails to stimulate domestic income because as much as 0.3 of the multiplier might leak out through extra imports.” (Anthony de Jasay, “Micro, Macro, and Fantasy Economics,” Library of Economics and Liberty, December 6, 2010)

2. The disincentivizing effects of government borrowing and spending

Even if additional debt does not crowd out private-sector borrowing to finance business expansion, it will nevertheless inhibit investments in business expansion. This inhibiting effect is compounded by the reasonable expectation that many items in a “stimulus” package will become permanent fixtures in the government’s budget

3. The timing-targeting problem

The lag between the initial agitation for “stimulus” and its realization. In the extreme, the lag can be so great as to have no effect other than to divert employed resources from private to government uses. But even where there is a relatively brief lag, “stimulus” spending is essentially wasted if the result is simply to divert already employed resources from private to government uses.

4. Inadequate Aggregate Demand (AD) is a symptom, not a cause

A drop in AD usually is caused by an exogenous event, and that exogenous event usually is a credit crisis. Pumping money into the economy — especially when it results in the bidding up the prices of already employed resources — does not reinflate the punctured credit bubble that caused the slowdown.

5. Inequity, moral hazard, and their consequences

Favorable treatment of defaulters and failing companies generates considerable popular resentment, which — in the present instance — has found a vocal and politically potent outlet in the Tea Party movement. Favorable treatment of defaulters and failing companies also creates moral hazard; that is, it encourage unwise risk-taking that can (and probably will) spark future crises, leading the government to assume more obligations and impose more regulations, in a futile effort to change human nature.

6. The human factor

Those who cling to the Keynesian multiplier would like the world to comply with it. But the world does not because it is filled with people, whose behavior is not determined (or described) by a simplistic model but by their responses to incentives, their political predispositions, their informed and reasonable skepticism about the consequences of government intervention in economic matters, and — above all else — their fallibility.

In truth, the Keynesian multiplier is a mathematical fiction, as explained here, and government spending is in fact destructive of economic growth, as discussed here and in some of the posts listed at the end.

“We owe it to ourselves” is a phrase used by Paul Krugman (among others on the left). It is a variant of the stock rationale for socializing gains and losses: “We’re all in this together.” As if the citizens of the United States were members of an extraordinarily large community, with a perpetual town-hall meeting conducted by the government of the United States.

Consider the intellectual dishonesty of Krugman’s claim that “we” owe the debt of the U.S. government to “ourselves.” Who are “we”? If government borrows money and spends it on goodies for Congressman X, Y, and Z’s districts, how do I get my cut? Or does the happiness generated in Congressman X, Y, and Z’s districts simply radiate in waves across the country, eventually reaching me and making me feel better?

If the borrowed money makes (some) people in Congressman X, Y, and Z’s districts better off, why is it that “we” (i.e. the rest of us and/or our descendants) end up repaying the debt that made those others better off? I do not understand how I “owe it to myself” when (a) I didn’t ask to borrow the money and (b) I gained nothing as a result of the borrowing.

You might claim that my personal wishes are of no account because Congress and the president are duly elected by majorities of voters. But that is tantamount to saying that Congress and the president possess a kind of omniscient super-consciousness that somehow overrides the harm, hate, and discontent that flow from their acts.

The left succeeds, in large part, because apologists for big government — from Krugman to Obama — are skillful practitioners of slippery logic. An assumption here, an assumption there, and government spending is made out to be a source of enrichment. The hard truth is that government spending — and the big government that it supports — is the source of America’s impending impoverishment.

Related posts:

Trade Deficit Hysteria

Trade, Government Spending, and Economic Growth

The Causes of Economic Growth

In the Long Run We Are All Poorer

A Short Course in Economics

Addendum to a Short Course in Economics

The Price of Government

Gains from Trade

The Price of Government Redux

The Indivisibility of Economic and Social Liberty

Trade

The Mega-Depression

As Goes Greece

Ricardian Equivalence Reconsidered

The Real Burden of Government

Toward a Risk-Free Economy

Enough of “Social Welfare”

Subjective Value: A Proof by Example

Microeconomics and Macroeconomics

The Illusion of Prosperity and Stability

Society and the State

I Want My Country Back

Estimating the Rahn Curve: Or, How Government Inhibits Economic Growth

Our Enemy, the State

“Intellectuals and Society”: A Review

Subjective Value: A Proof by Example

The Stagnation Thesis

Taxing the Rich

More about Taxing the Rich

Does World War II “Prove” Keynesianism?

Money, Credit, and Economic Fluctuations

A Keynesian Fantasy Land

The Keynesian Fallacy and Regime Uncertainty

Creative Destruction, Reification, and Social Welfare

Why the “Stimulus” Failed to Stimulate

The “Jobs Speech” That Obama Should Have Given

Say’s Law, Government, and Unemployment

Regime Uncertainty and the Great Recession

Regulation as Wishful Thinking

The Real Multiplier

Vulgar Keynesianism and Capitalism

Why Are Interest Rates So Low?

Merit Goods, Positive Rights, and Cosmic Justice

The Commandeered Economy

We Owe It to Ourselves

Estimating the Rahn Curve: A Sequel

The Real Multiplier (II)

Lay My (Regulatory) Burden Down

The Burden of Government

Economic Growth Since World War II

More Evidence for the Rahn Curve

“Big SIS”: A Review

The Capitalist Paradox Meets the Interest-Group Paradox

Progressive Taxation Is Alive and Well in the U.S. of A.

The Obama Effect: Disguised Unemployment

Some Thoughts about Leftist Hypocrisy

The State as Jailer

Where We Are, Economically