This post updates “The Fed and Business Cycles” of June 11, 2011.

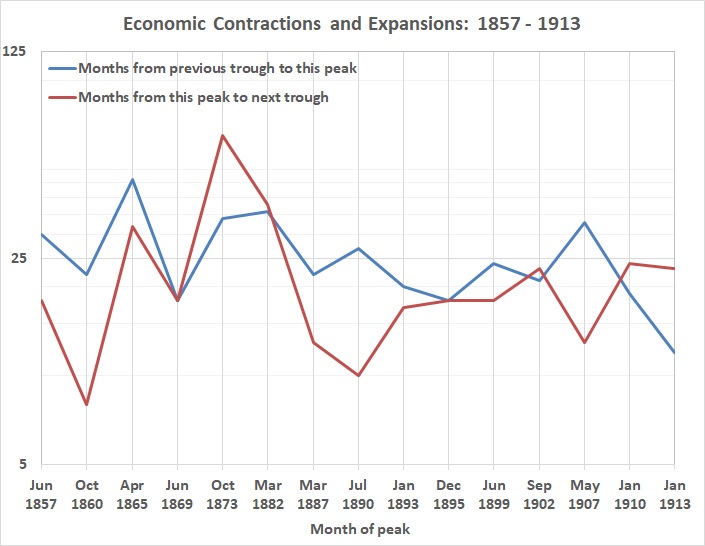

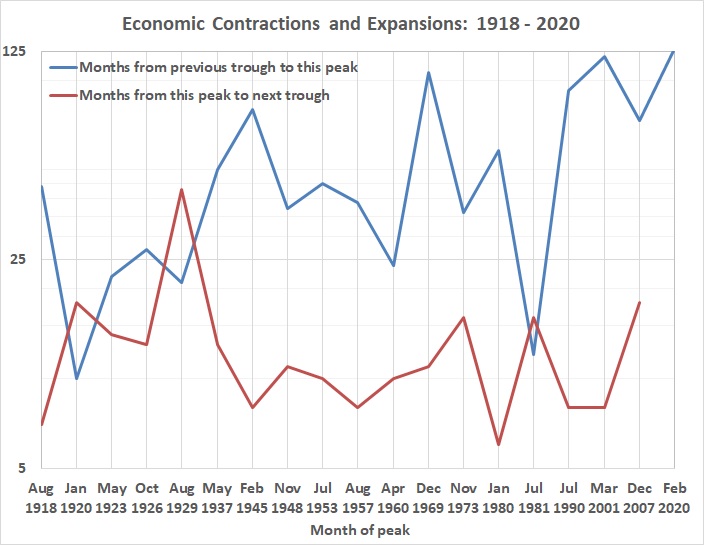

The following graphs depict the length of expansions and contractions (and the trends in both), before and since the creation of the Federal Reserve System in December 1913.

Source: “Business Cycle Expansions and Contractions,” National Bureau of Economic Research.

Note: The logarithmic scale on the vertical highlights proportional changes in the lengths of business cycles.

The creation of the Fed might have had a hand in the lengthening of expansions and the shortening of contractions, but many other factors have been at work.

What the graphs don’t depict is the relative severity of the various contractions. It is worth noting that the worst of them all — the Great Depression — occurred after the creation of the Fed and, in part, because of actions taken by the Fed. (A note to the history-challenged: The Great Depression began in September 1929 and ended only because of America’s entry into World War II.) Moreover, the worst downturn since the Great Depression — the Great Recession — was clearly the work of the Fed, in unwitting(?) complicity with the politicians who insisted on expanding home ownership through subprime loans.

In any event, the long-run cost of economic stability has been high. (See this, this, and this, for example.)