Russ Roberts wonders about the meaning of “pent up” demand:

The usual way that Keynesians explain the post-[World War II] expansion despite the huge cut in government spending is to say, well of course the economy boomed, there was a lot of pent-up demand. What does that mean? There is always pent-up demand in the sense there is a stuff I wish I could have but can’t. But the standard story is that people couldn’t buy washing machines or cars during the war–they were rationed or simply unavailable or unaffordable. So when the war ended, and rationing and price controls ended, people were eager to buy these things. But the reason these consumer goods were rationed or unavailable is because all the steel went into the tanks and planes during the war. So when the war ended, there was steel available to the private sector. That’s why cutting government activity can stimulate the private sector. Fewer resources are being commandeered by the public sector.

Roberts refers to an earlier post of his, in which he rightly ridicules Keynesians for believing in the magical multiplier:

One of the most mindless aspects of the multiplier is to treat is as a constant, such as 1.52. It can’t be a constant, not in any meaningful way. If the government conscripted half of the US population to dig holes all day and conscripted the other half to fill them back in, and paid each of us a billion dollars a day for the task, and valued holes that were dug and holes that were filled in at a trillion dollars a hole, then GDP would be very very large, unemployment would be zero and there would be no stimulating effect and we would soon be dead from starvation.

Priceless.

I share Roberts’s disdain for the multiplier. (See this and this.)

Nevertheless, the availability of resources for private use after the war ended is only half the story. Consumers and businesses had to demand things — not just want them, but demand them with money in hand. That is where pent-up demand comes into play, as I explain here:

Conventional wisdom has it that the entry of the United States into World War II caused the end of the Great Depression in this country. My variant is that World War II led to a “glut” of private saving because (1) government spending caused full employment, but (2) workers and businesses were forced to save much of their income because the massive shift of output toward the war effort forestalled spending on private consumption and investment goods. The resulting cash “glut” fueled post-war consumption and investment spending.

Robert Higgs, research director of the Independent Institute, has a different theory, which he spells out in “Regime Uncertainty: Why the Great Depression Lasted So Long and Why Prosperity Resumed After the War” (available here), the first chapter his new book, Depression, War, and Cold War. (Thanks to Don Boudreaux of Cafe Hayek for the pointer.) Here, from “Regime Change . . . ” is Higgs’s summary of his thesis:

I shall argue here that the economy remained in the depression as late as 1940 because private investment had never recovered sufficiently after its collapse during the Great Contraction. During the war, private investment fell to much lower levels, and the federal government itself became the chief investor, directing investment into building up the nation’s capacity to produce munitions. After the war ended, private investment, for the first time since the 1920s, rose to and remained at levels sufficient to create a prosperous and normally growing economy.

I shall argue further that the insufficiency of private investment from 1935 through 1940 reflected a pervasive uncertainty among investors about the security of their property rights in their capital and its prospective returns. This uncertainty arose, especially though not exclusively, from the character of federal government actions and the nature of the Roosevelt administration during the so-called Second New Deal from 1935 to 1940. Starting in 1940 the makeup of FDR’s administration changed substantially as probusiness men began to replace dedicated New Dealers in many positions, including most of the offices of high authority in the war-command economy. Congressional changes in the elections from 1938 onward reinforced the movement away from the New Deal, strengthening the so-called Conservative Coalition.

From 1941 through 1945, however, the less hostile character of the administration expressed itself in decisions about how to manage the warcommand economy; therefore, with private investment replaced by direct government investment, the diminished fears of investors could not give rise to a revival of private investment spending. In 1945 the death of Roosevelt and the succession of Harry S Truman and his administration completed the shift from a political regime investors perceived as full of uncertainty to one in which they felt much more confident about the security of their private property rights. Sufficiently sanguine for the first time since 1929, and finally freed from government restraints on private investment for civilian purposes, investors set in motion the postwar investment boom that powered the economy’s return to sustained prosperity notwithstanding the drastic reduction of federal government spending from its extraordinarily elevated wartime levels.

Higgs’s explanation isn’t inconsistent with mine, but it’s incomplete. Higgs overlooks the powerful influence of the large cash balances that individuals and corporations had accumulated during the war years. It’s true that because the war was a massive resource “sink” those cash balances didn’t represent real assets. But the cash was there, nevertheless, waiting to be spent on consumption goods and to be made available for capital investments through purchases of equities and debt.

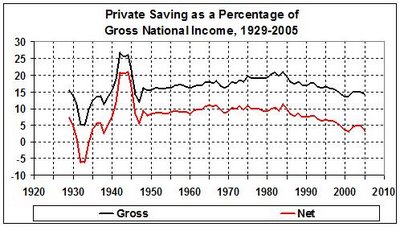

It helped that the war dampened FDR’s hostility to business, and that FDR’s death ushered in a somewhat less radical regime. Those developments certainly fostered capital investment. But the capital investment couldn’t have taken place (or not nearly as much of it) without the “glut” of private saving during World War II. The relative size of that “glut” can be seen here:

Derived from Bureau of Economic Analysis, National Income and Product Accounts Tables: 5.1, Saving and Investment. Gross private saving is analagous to cash flow; net private saving is analagous to cash flow less an allowance for depreciation. The bulge in gross private saving represents pent-up demand for consumption and investment spending, which was released after the war.World War II did bring about the end of the Great Depression, not directly by full employment during the war but because that full employment created a “glut” of saving. After the war that “glut” jump-started

- capital spending by businesses, which — because of FDR’s demise — invested more than they otherwise would have; and

- private consumption spending, which — because of the privations of the Great Depression and the war years — would have risen sharply regardless of the political climate.

The post continues with an exchange between Higgs and me. The bottom line is the same.

What is the answer to the title question, then? It is that a period of forced, nominal saving can create pent-up demand, which can result in the employment of resources that had theretofore been unavailable. The pent-up demand at the end of World War II was, in great measure, responsible for the post-war recovery.

This rare phenomenon has nothing to do with the multiplier, and probably has nothing to do with the current economic situation. Government has commandeered a large chunk of the American economy, but so gradually that Americans have not acquire a “glut” of nominal savings, as they did in World War II.