Executive Summary

One reason for continued economic growth and the resurgence of productivity is the trade deficit, which is not a form of debt. A trade deficit offsets government spending and therefore alleviates the “crowding out” effect that government spending has on private-sector consumption and investment. American consumers and businesses are better off than they would be in the absence of a trade deficit. For the trade deficit is nothing more than a manifestation of voluntary exchange, which — by definition — benefits both parties. In the case of international trade, foreigners (on net) are selling us goods and services while we are selling them a combination of goods, services, stocks, bonds, and mortgages. The so-called deficit, then, is nothing more than foreigners’ purchases of U.S. stocks, bonds, and mortgages.

Thus, instead of using resources to produce goods and services and sending them overseas in exchange for goods and services of equal value, some resources remain in the U.S. And some of those resources are then converted into capital investments that help make American businesses more productive and profitable. In effect, some foreigners are using the income they receive from Americans to “invest in America,” just as some Americans use some of their income to “invest in America.” There is no difference.

Nevertheless, when there is a trade deficit we are treated to gloom-and-doom-saying about “foreign “ownership” of U.S. assets and the “exportation” of American jobs. But foreign ownership of U.S. assets is not a threat to Americans; rather, it gives foreigners a stake in America’s economic growth. The threat of job “exportation” is just as bogus; when foreigners “do jobs that Americans could be doing” they are enabling Americans to make more productive use of their abilities. If you don’t care (and you shouldn’t) whether your car in made in Detroit or Tennessee, why should you care whether a computer technician works in the U.S. or overseas? What you should care about is the value you receive when you buy a car or use a computer help line.

The real villain of the piece is government spending, not government deficits. Government deficits are simply the result of government spending. It is government spending — not government borrowing — that threatens Americans’ prosperity.Through spending (whether it is financed by taxes or borrowing), government confiscates resources and puts them to generally wasteful and counterproductive uses.

Where does the trade deficit fit in? It doesn’t create government spending or government deficits. To the contrary, the trade deficit helps to offset the essential wastefulness of government spending by enabling Americans to enjoy and benefit from goods and services that government spending deprives them of.

You will come to understand the logic of these conclusions if you can bear with the bit of simple algebra that lies ahead. But first . . .

Some Background

The “real” economy — the economy that produces and uses goods and services — is healthy (though not as robust as it could be) in spite of (and not because of) government spending and regulatory activity. Although real GDP continues to grow at a lower rate than it did before the advent of the regulatory-welfare state about 100 years ago (Figure 1), the resurgence of productivity (Figure 2) offers hope for the future.

Figure 1

Source and explanation: “The Destruction of Income and Wealth by the State.”

Figure 2

Source and explanation: “Productivity Growth and Tax Cuts.”

As Figure 2 suggests, the so-called boom of the 1990s really began in the early 1980s, as inflation was tamed and Reagan’s tax cuts and pro-business attitude gave new hope to inventors, innovators, and entrerpreneurs — and to those who finance them. It is those economic actors, not government, who are responsible for economic growth. The best thing government can do, when it comes to the economy, is to get out of the way.

When I say “get out of the way” I am not talking about reducing government deficits. Nor am I talking about eliminating the so-called trade (or current-account) deficit, which many commentators see (wrongly) as a cause of government budget deficits. Government spending is the real obstacle to robust economic growth. It is a drag on the economy because it diverts resources to what are mainly nonproductive activities. Moreover, government regulatory programs have a cumulative, counterproductive effect that is out of proportion to their cost because the regulatory burden on business activity keeps piling up. (Refer again to Figure 1, and go to the source for the depressing details.)

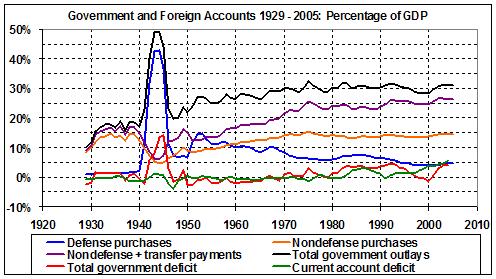

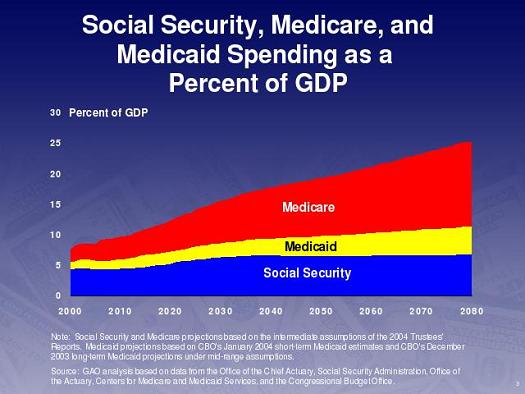

Figure 3 (which encompasses spending and deficits at all levels of government) provides some needed perspective. Notice the historical disconnect between the government deficit and the current-account deficit. The fact that both have been rising in recent years is a coincidence, about which many commentators have drawn the wrong inference. The “500-pound gorilla” in Figure 3 is government spending, in particular, the growing burden of transfer payments (e.g., Social Security, Medicare, and Medicaid), which take from those who produce and give to those who do not, and which discourage saving and encourage consumption. The rise in transfer payments has kept total government outlays above 30 percent of GDP since 1970. Figure 4 indicates that the situation is likely to worsen considerably, given current “commitments” to Social Security, Medicare, and Medicaid.

Figure 3

Sources: Bureau of Economic Analysis, National Economic Accounts, Table 1.1.5. Gross Domestic Product (lines 1, 20-24), Table 3.1. Government Current Receipts and Expenditures (lines 17, 29), Table 4.1 Foreign Transactions in the National Income and Product Accounts (line 29).

Figure 4

Source: Government Accounting Office (see also “Funding the Welfare State“).

This recitation of dreary facts sets the stage for the rest of this post, which focuses on the real problem, which is government spending — not government deficits (per se), and certainly not the so-called trade deficit.

The “Real” Economy in Simple Formulae

The following formulations depict the “real” economy at a given time. (See this article for a more complex but equivalent depiction.) These formulations do not, by themselves, depict the dynamics of economic growth or the cause-and-effect relationships among the various parameters of the real economy. I supply some of those missing ingredients in the commentary that follows.

The totality of real economic activity can be expressed as an identity:

(1) Income ≡ Output

That is, aggregate income (the claims on or distribution of output) must be equal to the aggregate of all types of output.

Income and output can be expressed in terms of certain parameters:

(2.a) Income = C + S + T + M

(2.b) Output = C + I + G + X ,

where the parameters are defined as follows:

C = consumption (private-sector consumption of goods and services produced domestically, excluding consumption that is subsidized by government transfer payments to the beneficiaries of such programs Social Security and Medicare)

S = saving (private-sector income not consumed, taxed, or spent on imports)

I = private-sector investment (output invested by non-governmental entities in technology, buildings, equipment, etc., for the purpose of increasing the future output of goods and services)

M = items imported for private-sector consumption or investment from other countries

X = private-sector output exported to other countries

T = taxes, including transfer-payment taxes for Social Security, etc.

G = government spending (including spending that is subsidized by transfer payments for such programs as Social Security and Medicare)

and:

(X – M) or (M – X) = trade surplus or deficit

(T – G) or (G – T) = government surplus or deficit.

These definitions vary from the standard version in that any spending subsidized by government transfer payments for such programs as Social Security and Medicare is included in G rather than C . These definitions also implicitly reject a role for government in saving and investment, for reasons spelled out in my post, “Joe Stiglitz, Ig-Nobelist.”

Key Relationships

Because Income ≡ Output, it follows that:

(3) C + S + T + M = C + I + G + X

In a closed economy without government the Income ≡ Output identity reduces to this:

(3′) C + S = C + I

Given that C ≡ C, it follows that S = I in a closed economy without government.That is, absent government (which usurps saving through taxation), the backbone of private-sector investment is private-sector saving.

In an open economy without government the Income ≡ Output identity becomes this:

(3”) C + S + M = C + I + X

Given that C ≡ C, it follows that (S + M) = (I + X) in an open economy without government. That is, given a level of exports, the backbone of private-sector investment is the combination of private-sector saving and imports that are not consumed. It therefore follows that . . .

The Trade Deficit Is Good

Solving 3 for (M – X), the trade deficit, we get:

(4) (M – X) = (I – S) + (G – T)

What (4) tells us is that a trade deficit is a boon to economic growth. That is, an increase in M (or a decrease in X) supports an increase in I , even when T reduces S .

Consider, for example, an exogenous increase in M (e.g., because of economic growth or a drop in the prices of imported goods relative to the prices of domestic substitutes). An exogenous increase in M means that more resources become available for I (as well as C). By the same token, an exogenous decrease in X (e.g., because a rise in U.S. interest rates attracts foreign money away from U.S. exports and toward U.S. bonds and mortgages) means that more resources become available for I (as well as C).

In sum, the causality runs from trade. Trade is an enabler. Foreign trade is just another form of voluntary exchange, which benefits all parties. In the case of foreign trade, Americans stand to capture real resources that can be invested in growth-producing capital. The so-called trade deficit isn’t the “bad” side of trade, it’s the good side of trade.

The catch is that government may confiscate some of the potential gains from a trade deficit by adding to its debt when G is greater than T . Which leads me to this . . .

A Trade Deficit Is Not a Form of Debt

Solving (3) for (G – T), we get:

(5) (G – T) = (S – I) + (M – X).

It is apparent that a trade deficit can finance a portion of the government deficit. That is why government-deficit and trade-deficit hysterics liken the trade deficit to a form of debt — which it is not. The trade deficit does not create the government deficit. The government deficit arises mainly from exogenous decisions about the size of G and the various taxes that result in T .

To repeat and elaborate: The trade deficit — when there is one — merely helps to finance the government deficit — when there is one. The two are essentially independent of each other. Consider an increase in the trade deficit, which enables an increase in private investment and/or consumption (see the preceding section). The government may (through taxing or borrowing) confiscate some or all of the increase in the trade deficit. Thus a trade deficit, which is potentially beneficial because it enables an increase in private investment, simply “soaks up” some of the government deficit. But the trade deficit is merely coincidental with the government deficit, and is not created by it.

In the absence of a trade deficit, the burden of a government deficit would fall entirely on the domestic private sector. For example, referring to (5), in the absence of a trade deficit, an increase in G would require an offsetting reduction in I (as well as C). (It would be ludicrous to interpret (5) as saying that an increase in G leads to an increase in S .)

In other words, a trade deficit makes things better for the private sector — not worse — and the trade deficit has nothing to do with the size of the government deficit. The coincidental rise of the government deficit and the trade deficit in recent years (Figure 3) is just that: coincidental. Anyone who says that the trade deficit is a form of debt is guilty of (a) mistaking coincidence for causality, and (b) misunderstanding the meaning of “deficit” in the term “trade deficit.”

There is no trade deficit. The things foreigners buy from us have exactly the same value as the things we buy from them. The mix of things foreigners buy from us simply happens to include a higher proportion of stocks, bonds, and mortgages than the mix of things Americans buy from foreigners.

Bogus “Threats”: Foreign “Ownership” and “Job Exportation”

There is the notion that the holding of U.S. stocks, bonds, and mortgages gives foreigners a “hold” over us. How so? It hurts foreign holders of U.S. equities, securities, and real estate if those things lose value. Foreigners have absolutely no incentive to “dump” their holdings of U.S. financial instruments unless financial markets already have signaled that those instruments are losing value for reasons unrelated to the ownership of financial assets. Foreign “dumping” in a panic is no different than “dumping” by domestic holders of financial assets. Anyone can panic; Americans have no monopoly on steadfastness when it comes to financial markets.

A foreign investor who “dumps” U.S. paper simply out of pique would be the loser because the investor would be driving down the value of the very holdings it wishes to “dump.” The value of the “dumped” holdings would return to something like their former levels once the investor had finished “dumping,” thus rewarding the buyers with windfall profits.

As for “job exportation,” I must quote from a post I wrote several months ago:

Outsourcing, which is really the same thing as international trade, creates jobs, creates wealth, and raises real incomes — for all. Economics is a positive-sum “game.”

If you’re not convinced, think of it this way: If product X is a good value, does it matter to you whether it was made in Poughkeepsie or Burbank? Well, then, there’s nothing wrong with Laredo, Texas, or Calais, Maine, is there?

Now imagine that the Rio Grande River shifts course and, poof, Nuevo Laredo, Mexico, becomes Nuevo Laredo, Texas. Or suppose that the Saint Croix River between Maine and New Brunswick, shifts course and the former St. Stephen, New Brunswick, becomes St. Stephen, Maine. Juan and Pierre are now Americans. Feel better?

What’s in a border? A border is something to be defended against an enemy. But do you want a border to stand between you and lower prices, more jobs, and economic growth? I thought not.

Taxes Always Hurt

Solving (3) for I , we get:

(6) I = S + (T – G) + (M – X)

That is, private-sector investment is equal to private-sector saving, plus the government surplus (or minus the government deficit), plus the trade deficit (or minus the trade surplus). I re-emphasize: plus the trade deficit (see “The Trade Deficit Is Good,” above).

Equation (6) might be (and has been) taken to mean that a tax increase would lead to an increase in private-sector investment. (That ludicrous assertion is owed to “Rubinomics” — the true “voodo economics.”) Remember, however, that a tax increase must be financed by a decrease in C, S, or M (or some combination of them). A tax increase almost certainly will cause a decrease in I because I depends largely on S and (M – X). Equation (6) is best understood this way: Given the level of T and G , I rises (or falls) with S and the trade deficit (M – X).

When the economy continues to grow in the wake of a tax increase it is because the forces underlying private-sector growth (e.g., returns on prior investments) are sufficiently strong to overcome the inhibiting effects of the tax increase. Think of the economy as a healthy child. Think of a tax increase as a common cold. The cold will cause the child to have less energy than usual, but it will not cause the child to stop growing. On the other hand, too many colds — like too much taxation — can take their toll and turn a healthy child into a sickly one who never fulfills his potential. (See Figure 1 again, and visit the source for it, if you haven’t already done so.)

Government Spending Always Hurts (with a Few Exceptions)

Recall (2.b)? This is what follows from it:

If G goes up, C, I, or X — or a combination of them — must go down.

The key parameter is I , which represents new technology, buildings, equipment, software, etc. — all of which yield more jobs and higher incomes. (By the way, G is not a viable alternative to I ; don’t even consider it.) But X is important, too, because exports enable us to exchange goods and services with foreigners, to our mutual benefit. In sum, G confiscates resources that could have gone into I and X (not to mention C). G also supports the accretion of burdensome regulations.

G is good only when it supports defense and justice. Defense is an insurance policy for our lives, liberty, and property. Justice is that, too, and it also promotes the kind of orderly environment that enables economic activity to thrive.

It follows that the real threat to the well-being of Americans isn’t government deficits (per se) or trade deficits or foreign holdings of U.S. stocks and bonds. The real threat is government spending. Whether government spending is financed by debt or taxes, it is a generally destructive force. Government spending (with exceptions for defense and justice) results in the gross misuse of resources. Beyond that, government spending on regulatory activities inhibits growth-producing investments and blunts the productivity of those investments that are made. And the ways in which Americans are taxed to fund government spending (most of it is funded by taxes) tends to penalize, and thus discourage, invention, innovation, and entrepreneurship. I once estimated the cost to Americans of the regulatory-welfare state that has become dominant over the past 100 years:

- Real GDP (in year 2000 dollars) was about $10.7 trillion in 2004.

- If government had grown no more meddlesome after 1906, real GDP might have been $18.7 trillion [Figure 1].

- That is, real GDP per American would have been about $63,000 (in year 2000 dollars) instead of $36,000.

- That’s a deadweight loss to the average American of more than 40 percent of the income he or she might have enjoyed, absent the regulatory-welfare state.

That loss is in addition to the 40-50 percent of current output which government drains from the productive sectors of the economy [the direct burden of taxes, plus the direct costs of regulatory compliance].

Those vast losses of income have resulted in vast losses of wealth; for example (from the same post):

[T]he stocks of corporations in the S&P 500 are currently undervalued by one-third because of the depradations of the regulatory-welfare state, which have lowered investors’ expectations for future earnings. . . .

And that’s only the portion of wealth that’s represented in the S&P 500. Think of all the other forms in which wealth is stored: stocks not included in the S&P 500, corporate bonds, mortgages, home equity, and so on.

If government had left its grubby hands off the economy, there never would have been a Great Depression, Social Security, Medicare, Medicaid, and the myriad regulations that have us tied in knots.

And we would be vastly better off.

Our “leaders” in Washington obviously don’t want to do much of anything to cope with the real threat to our well-being. They’re like terminal alcoholics who keep ordering triple shots.

“Crowding Out” in Perspective

What about the notion that government deficits “crowd out” private-sector investment? In a growing economy — both national and global — government spending rises alongside private-sector investment because there is room for both to grow. We would be better off with decreases in most kinds of government spending (excepting defense and justice). But we would be better off because government would be confiscating fewer resources that could go into consumption and growth-producing investments. It’s not government deficits (per se) that matter; it’s government spending that matters. Government deficits are a drop in the proverbial bucket of global liquidity. To quote myself again:

The crowding-out hypothesis . . . is based on a static analysis — a mere truism — which says that a given level of national output can be reallocated, but not changed. But the crowding-out hypothesis, which has reputable critics and doubters (see here, here, here, and here, for instance) doesn’t apply to a dynamic economy. The actual effect of government borrowing on interest rates — and thus on the cost of private capital formation — is minuscule, and perhaps nonexistent, as Brian S. Westbury explains:

The theory [that deficits drive up interest rates] suggests that deficits “crowd out” private investment, putting upward pressure on interest rates. In other words, government borrowing eats up the available pool of capital. But today’s forecasted deficits of $300 to $500 billion are just a small drop in the pool of global capital markets. In the U.S. alone, capital markets are $30 trillion dollars deep, for the world as a whole they approach $100 trillion. Deficits of the size projected in the years ahead cannot possibly have the impact on interest rates that many fear. . . .

The trade deficit — fortunately — blunts the confiscatory effects of government spending. Why? Because if foreigners aren’t spending all the dollars they earn on U.S. produced goods and services, it means that they are buying U.S securities, equities, and mortgages. That is, they are enabling private-sector investments that help to make American businesses more productive and profitable.

Net foreign buying of U.S. securities, equities, and mortgages also has been a major cause of the decade-long decline in U.S. interest rates. (See, for example this, this, and this.) American stockholders and homebuyers are therefore “indebted” to foreigners who buy U.S. stocks and bonds. American bondholders (on the whole) also have gained because rising bond prices have more than offset the decline in interest rates.

What Does the Future Hold?

There is no reason to believe that rising interest rates will cause the net inflow of foreign funds to dry up. Rising interest rates might cause foreigners to shift from stocks to bonds, but rising interest rates will attract money from abroad, not repel it. Even if the net inflow of foreign funds were to slow down for some reason, it is not going to suddenly dry up. And even if it dries up eventually, it won’t dry up forever because — in the world of economics — nothing is forever. A trend usually creates the conditions for its reversal:

We’ve been through periods of high inflation, high interest rates, large trade deficits, and low exchange rates at varying times, and we’ll go through them again. Today we have relatively low (but rising) inflation, and relatively low (but rising) interest rates, a persistently large trade deficit (willingly financed by foreigners), and therefore a falling exchange rate. But all of that can and will change as higher interest rates and lower exchange rates work their way through the economy, dampening investment and consumption spending and, therefore, imports.

Today is not forever. Doomsaying is an ancient and long-discredited profession. Remember the ten years between the “oil shocks” of the early 1970s and the end of double-digit inflation in the early 1980s? Remember the next 20 years of almost unmitigated economic growth with low inflation? Extrapolating from current economic conditions is a sucker’s game, unless you bet on the underlying trend in the U.S., which is long-term economic growth.

In any event, future changes in the net inflow of foreign funds cannot undo the benefits that have accrued to Americans because of past inflows. Those who fear a “drying up” of the inflow are like bums who have been getting free meals and then complain when the soup kitchen shuts down. You take what you can get, when you can get it, and invest it wisely. That’s evidently what Americans have been doing, thanks to the trade deficit — and no thanks to government spending.

Related posts:

The Destruction of Income and Wealth by the State

Why Outsourcing Is Good: A Simple Lesson for Liberal Yuppies

Curing Debt Hysteria in One Easy Lesson

Trade Deficit Hysteria

Brains Sans Borders

Understanding Economic Growth

The Real Meaning of the National Debt

Debt Hysteria, Revisited

Why Government Spending Is Inherently Inflationary

Understanding Outsourcing

Joe Stiglitz, Ig-Nobelist

Professor Buchanan Makes a Slight Mistake

More Commandments of Economics

Productivity Growth and Tax Cuts

Do Future Generations Pay for Deficits?

Liberty, General Welfare, and the State

Starving the Beast, Updated