ADDENDUM BELOW

Scott Sumner has some thoughts on the subject. Sumner debunks the bubble-prediction prowess of Robert J. Shiller, and concludes with this:

[Shiller’s] stock market model has done very poorly since 2010, when his model suggested the S&P500 was 20% overvalued. At the time it was at 1070! [It closed on Friday, August 30, at 2003.]

We all make either implicit or explicit forecasts about the markets. If we later notice market movements that seem to align with our initial forecasts we tend the pat ourselves on the back and assume the forecasts were correct. This is just one of many cognitive biases that we human beings are prone to. My suggestion is to pay no attention to bubble forecasts. They are useless. Indeed the entire bubble concept is useless.

Shiller’s model relies heavily on an indicator that he devised: CAPE-10 (10-year cyclically adjusted price-earnings ratio). A current graph and the underlying data can be found here.

One problem with CAPE-10 — though not the only problem — is knowing when the market is “too high.” What is the norm against which current stock prices should be evaluated? It seems that a lot of weight is given to the trend since January 1871, which is how far back Shiller has reconstructed the value of the S&P 500 Index. (He calls it the S&P Composite, which is a broader index of 1,500 stocks — but he uses values for the S&P 500.)

January 1871 is an arbitrary date, of course. There have been many trends in the intervening 143 years. Consider some of the trends that began in January 1871:

Of the trends shown in the graph, only the trend through 1901 and the trends through 1999 and the present have been positive. The current trend (heavy black line) is the longest. Does that make it “normal”? Well, “normal” will shift up and down as the series extends into the future.

Many other trends can be concocted; for example 1901-1920 (negative); 1920-1929 (positive); 1929-1932 (negative); 1932-1937 (positive); 1937-1942 (negative); 1942-1966 (positive); 1966-1982 (negative); 1982-1999-positive; and 1999-March 2014 (negative). Take your pick, or concoct your own.

When it comes to stock prices, a trend is a useless concept. It’s manufactured from hindsight, and has no predictive value.

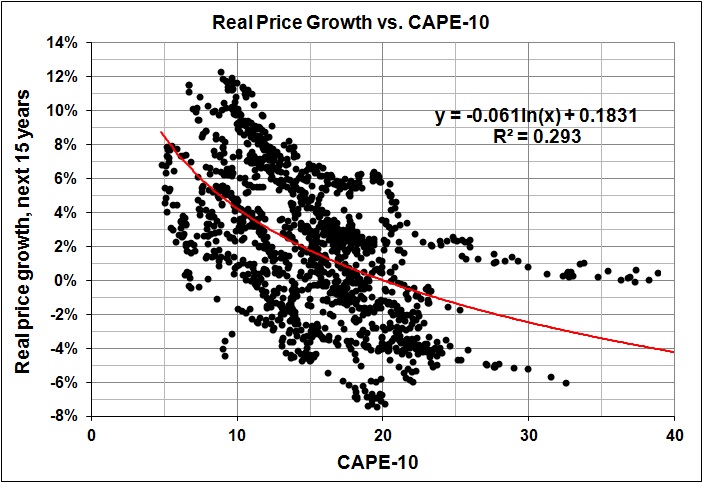

What about the relationship between CAPE-10 and price growth in subsequent years? Shiller made much of this in his non-prediction of 1996. (See his “Valuation Ratios and the Long-Run Stock Market Outlook.”) There is, as you might expect, a generally negative relationship between CAPE-10 and subsequent stock-price returns.

But the relationship for 1871-2014 (shown above) is so loose as to be useless as a predictor. One might, as Shiller did, select a subset of the data and focus on the relationship for that subset, which is almost certain to be tighter than the relationship for the entire data set. But which subset should one choose? The correct answer — if there is one — becomes obvious only in hindsight. And by the time hindsight comes into play, the relationship will no longer hold.

I said it more than 30 years ago, and I stand by it: Trends were made to broken.

And we never know when they will break.

ADDENDUM (09/03/14):

The focus on stock prices is much ado about relatively little. The rate of real growth in the S&P index since January 1871 is 1.8 percent a year. For the same period, he rate of real growth in the S&P index with dividends reinvested is 6.6 percent a year. Huge difference:

As of June 2014, the green line had increased 12,750-fold; the blue line, only 23-fold.

“Buy and hold” should be: Buy, reinvest dividends, and hold.