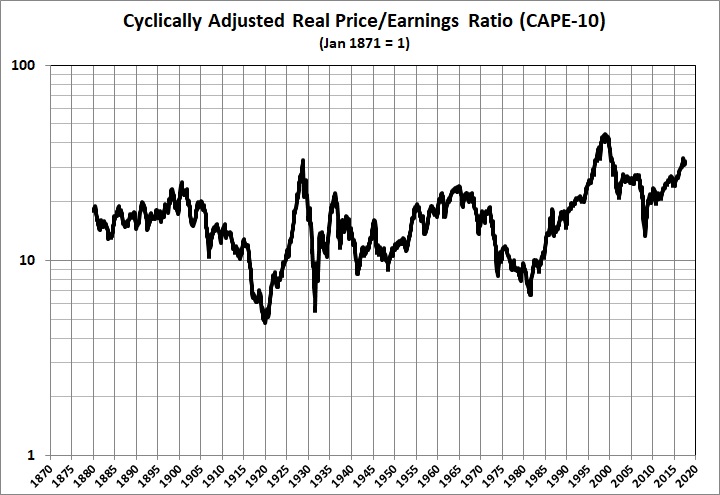

Does the long-term trend of the price-earnings ratio have an upward tilt? You might think so, if you encounter Robert Shiller’s Cyclically Adjusted Price-Earnings (CAPE) ratio for the S&P Composite. It looks like this:

Derived from Robert Shiller’s data set at http://www.econ.yale.edu/~shiller/data/ie_data.xls.

The plot begins in January 1881 and extends through October 2012. As explained here, CAPE is supposed to more accurately reflect the value of stocks:

Legendary economist and value investor Benjamin Graham noticed the … bizarre P/E behavior during the Roaring Twenties and subsequent market crash. Graham collaborated with David Dodd to devise a more accurate way to calculate the market’s value, which they discussed in their 1934 classic book, Security Analysis. They attributed the illogical P/E ratios to temporary and sometimes extreme fluctuations in the business cycle. Their solution was to divide the price by a multi-year average of earnings and suggested 5, 7 or 10-years. In recent years, Yale professor Robert Shiller, the author of Irrational Exuberance, has reintroduced the concept to a wider audience of investors and has selected the 10-year average of “real” (inflation-adjusted) earnings as the denominator. As the accompanying chart illustrates, this ratio closely tracks the real (inflation-adjusted) price of the S&P Composite. The historic average is 16.4. Shiller refers to this ratio as the Cyclically Adjusted Price Earnings Ratio, abbreviated as CAPE….

CAPE can be quite misleading, however:

The problem with [the 10-year moving average of earnings] is that the typical or average business cycle has been significantly shorter than 10 years. According to data compiled by the National Bureau of Economic Research, economic contractions have become shorter and expansions longer in recent years. Furthermore, while the business cycle has lengthened in recent years, it is still considerably shorter than 10 years. Measured trough to trough, the average business cycle has been six years and one month for the most recent 11 cycles. Measured peak to peak, the average is five years and six months.

The problem with using a moving average that is longer than the business cycle is that it will overestimate “true” average earnings during a contraction and underestimate “true” average earnings during an expansion. According to the National Bureau of Economic Research, the last recession ended in June 2009 and the U.S. economy is now in an expansion phase. Thus, the average earnings estimate used by the July 2011 CAPE is too low and produces a bearishly biased estimate of value.

Using Shiller’s data, a July 2011 CAPE based on the average of six years of real earnings is 21.26 and the long-term average CAPE based on the average of six years of real earnings is 15.78. Comparison to this average indicates that stocks are overvalued by 34.7%. While still signaling that stocks are overvalued, the degree of overvaluation is much less than the 42.3% estimate provided by the July 2011 CAPE based on a 10-year average of real earnings.

When viewed correctly, then, the long-term P-E ratio for the S&P Composite (based on current earnings) looks like this:

Derived from Shiller’s data set. The vertical bars show variations of 1 standard error around the means for each of the three eras.

If I had fitted a long-term trend line through the entire series, it would tilt upward, as it does for CAPE. But that trend would be misleading because it would give undue weight to the stock-market bubble of the late 1990s and the artificially high P-E ratios resulting from the earnings crash during the Great Recession.

In fact, a trend line for the period 1871-1995 would be perfectly flat. Moreover, as shown in the graph immediately above, there is little difference between the first half of that period (1871-1933) and second half (1934-1995). The standard-error bars for both eras are almost the same height and vertically centered at almost the same value. The second era is just slightly (but insignificantly) more volatile than the first era.

As indicated by the standard-error bars, the P-E ratio for 1996-2012 is markedly higher than for the earlier eras. But, of late, the P-E ratio shows signs of returning to the normal range for 1871-1995.

In sum — and contrary to the story that is peddled by “bulls” — I doubt that the real long-term trend of the P-E ratio is upward. Rather, the apparent upward trend reflects bizarre happenings in the past 16 years: an unprecedented price bubble and a brief but steep earnings crash. I would therefore caution investors not to buy stocks in the belief that the P-E trend is upward. For reasons discussed here, the long-term trend of stock prices is more likely downward.

Related posts:

The Price of Government

The Price of Government Redux

The Mega-Depression

Ricardian Equivalence Reconsidered

The Real Burden of Government

The Rahn Curve at Work

The “Forthcoming Financial Collapse”

Estimating the Rahn Curve: Or, How Government Inhibits Economic Growth

The Deficit Commission’s Deficit of Understanding

The Bowles-Simpson Report

The Bowles-Simpson Band-Aid

The Stagnation Thesis

America’s Financial Crisis Is Now

Stocks for the Long Run?

Estimating the Rahn Curve: A Sequel

Bonds for the Long Run?

The Real Multiplier (II)

Lay My (Regulatory) Burden Down

Economic Growth Since World War II

More Evidence for the Rahn Curve

Progressive Taxation Is Alive and Well in the U.S. of A.

The Economy Slogs Along

The Obama Effect: Disguised Unemployment

The Stock Market as a Leading Indicator of GDP

Where We Are, Economically