Drawing on the database maintained by Robert Shiller, author of Irrational Exuberance, I estimated the constant-dollar value of the S&P Composite Index (S&P) with dividends reinvested. The validity of my estimate is confirmed by comparing it with the Wilshire 5000 Total Return Index (WLX), which is based on the reinvestment of dividends in the underlying stocks:

FIGURE 1

“Real” means that the underlying values are inflation-adjusted. The indices are equated to 1 in December 1970 because that is the first month of the WLX.

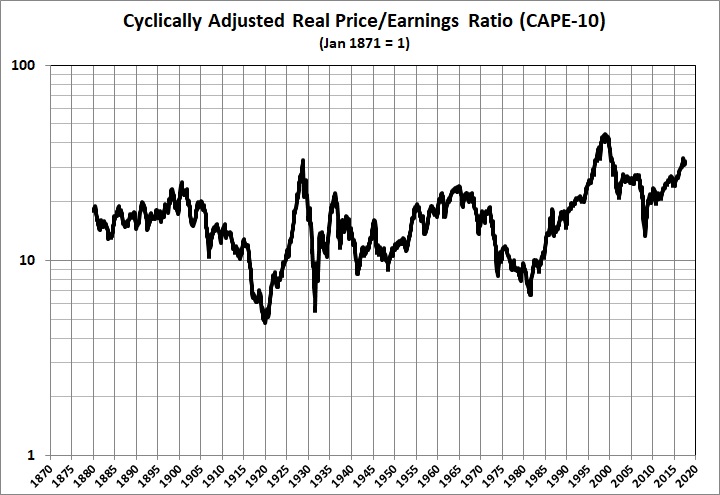

Shiller uses a cyclically adjusted price-earnings ratio (CAPE) based on the inflation-adjusted value of S&P and earnings on the constituent stocks. Specifically, he uses the current inflation-adjusted price divided by the average of inflation-adjusted earnings for the preceding 10 years. Accordingly, he calls it CAPE-10:

FIGURE 2

What is the relationship between the value of CAPE-10 for a particular month and the total return on the S&P over an extended period? Shiller’s database (which is reconstructed, of course) goes back to January 1871. January 1881 is therefore the date of his earliest CAPE-10 value. This graph shows the relationship between CAPE-10 and total returns for all 15-year periods beginning January 1881 and ending June 2018:

FIGURE 3

There’s an inverse relationship, as you would expect. But it’s a loose one because of marked shifts in the value of CAPE-10.

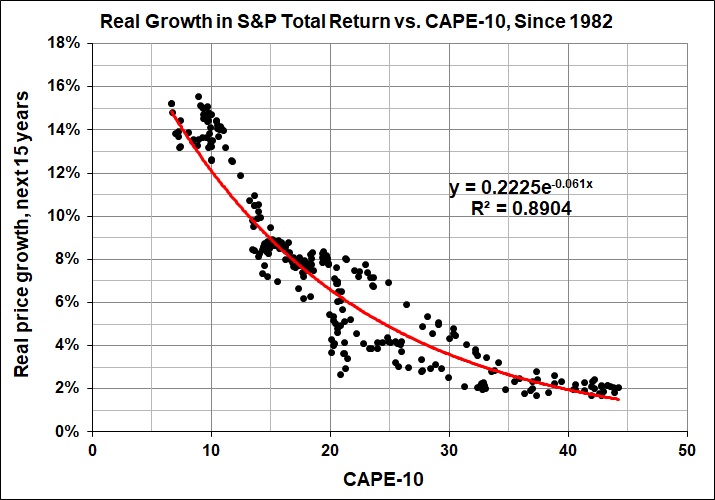

There’s a much tighter relationship for the “modern” financial era. I trace the beginning of this era to about 1982, when the stock market bottomed (see Figures 1 and 2) while inflation was receding from its post-World War II peak in 1980:

FIGURE 4

Here’s the relationship between CAPE-10 and real, annualized 15-year returns on the S&P since 1982:

FIGURE 5

The current value of CAPE-10 is about 32. If the relationship in Figure 5 holds true for the next 15 years, investors can expect real, annualized returns (with dividends reinvested) of 2 percent to 4 percent on broadly diversified mutual funds and stock portfolios.

Not great, you say? Well, the current real return on Baa-rated corporate bonds is about 1.5 percent. It’s less than that for Aaa-rated bonds, Treasury issues, most CDs, money-market funds, and deposit accounts. So if you’re into buy-and-hold, the stock market isn’t a bad bet. Alternatively, you can try to pick the next “big thing” — Tesla, for example.