This is a companion to “Richard Thaler, Nobel Laureate” and “Thaler’s Non-Revolution in Economics“. See also the long list of related posts at the end of “Richard Thaler, Nobel Laureate”.

Richard Thaler, the newly minted Noble laureate in economics, has published many papers, including one about discounting as a tool of government decision-making. The paper, “Discounting and Fiscal Constraints: Why Discounting is Always Right”, appeared in August 1979 under the imprimatur of the think-tank where Thaler was a consultant. It was also published in the October 1979 issue of the now-defunct Defense Management Journal (DMJ). Given the lead time for producing a journal, it’s almost certain that there is no substantive difference between the in-house version and the DMJ version. But only the in-house version seems to be available online, so the preceding link leads to it, and the quotations below are taken from it.

The aim of Thaler’s piece is to refute an article in the March 1978 issue of DMJ by Commander Rolf Clark, “Should Defense Managers Discount Future Costs?”. Specifically, Thaler argues against Clark’s conclusion that discounting is irrelevant in a regime of fiscal constraints.*

Clark took the position that a defense manager faced with fiscal constraints should simply choose among alternatives by picking the one with the lowest undiscounted costs. Why? Because the defense manager, unlike a business manager, can’t earn interest by deferring an expenditure and investing the money where it earns interest. To put it another way, deferring an expenditure doesn’t result in a later increase in a defense manager’s budget. Or in the budget of any government manager, for that matter.

Viewed in perspective, the dispute between Thaler and Clark is a tempest in a teaspoon — a debate about how to arrange the deck chairs on the Titanic. Discounting is of little consequence against this backdrop:

- uncertainty about future threats to U.S. interests (e.g., their sources, the weapons and tactics of potential enemies, and the timing of attacks)

- uncertainty about the actual effectiveness of U.S. systems and tactics (e.g., see this)

- uncertainty bout the costs of systems, especially those that are still in the early stages of development

- a panoply of vested interests and institutional constraints that must be satisfied (e.g., a strong Marine Corp “lobby” on Capitol Hill, the long dominance of aviation in the Navy, the need to keep the peace within the services by avoiding drastic changes in any component’s share of the budget)

- uncertainty about the amounts of money that Congress will actually appropriate, and the specific mandates that Congress will impose on spending (e.g., buy this system, not that one, recruit to a goal of X active-duty personnel in the Air Force, not Y).

But the issue is worth revisiting because it reveals a blind spot in Thaler’s view of decision-making.

Thaler begins his substantive presentation by explaining the purpose of discounting:

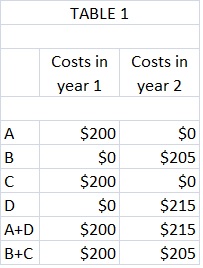

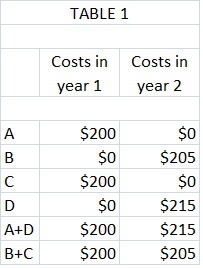

A discount rate is simply a shorthand way of defining a firm’s, organization’s, or person’s time value of money. This rate is always determined by opportunity costs. Opportunity costs, in turn, depend on circumstances. Consider the following example: An organization must choose between two projects which yield equal effectiveness (or profits in the case of a firm). Project A will cost $200 this year and nothing thereafter. Project B will cost $205 next year and nothing before or after. Notice that if project B is selected the organization will have an extra $200 to use for a year. Whether project B is preferred simply depends on whether it is worth $5 to the organization to have those $200 to use for a year. That, in turn, depends on what the organization would do with the money. If the money would just sit around for the year, its time value is zero and project A should be chosen. However, if the money were put in a 5 percent savings account, it would earn $10 in the year and thus the organization would gain $5 by selecting project B. [pp. 1-2]

In Thaler’s simplified version of reality, a government decision-maker (manager) faces a choice between two projects that (ostensibly) would be equally effective against a postulated threat, even though their costs would be incurred at different times. Specifically, the manager must choose between project A, at a cost of $200 in year 1, and project B, at a cost of $205 in year 2. Thaler claims that the manager can choose between the two projects by discounting their costs:

A [government] manager . . . cannot earn bank interest on funds withheld for a year. . . . However, there will generally exist other ways for the manager to “invest” funds which are available. Examples include cost-saving expenditures, conservation measures, and preventive maintenance. These kinds of expenditures, if they have positive rates of return, permit a manager to invest money just as if he were putting the money in a savings account.

. . . Suppose a thorough analysis of cost-saving alternatives reveals that [in year 2] a maintenance project will be required at a cost of $215. Call this project D. Alternatively the project can be done [in year 1] (at the same level of effectiveness) for only $200. Call this project C. All of the options are displayed in table 1.

[pp. 3-4]

Thaler believes that his example clinches the argument for discounting because the choice of project B (an expenditure of $205 in year 2) enables the manager to undertake project C in year 1, and thereby to “save” $10 in year 2. But Thaler’s “proof” is deeply flawed:

- If a maintenance project is undertaken in year 1, it will pay off sooner than if it is undertaken in year 2 but, by the same token, its benefits will diminish sooner than if it is undertaken in year 2.

- More generally, different projects cannot, by definition be equally effective. Projects A and B may be about equally effective by a particular measure, but because they are different they will differ in other respects, and those differences could be crucial in choosing between A and B.

- Specifically, projects A and B might be equally effective when compared quantitatively in the context of an abstract scenario, but A might be more effective in an non-quantifiable but crucial respect. For example, the earlier expenditure on A might be viewed by a potential enemy as a more compelling deterrent than the later expenditure on B because it would demonstrate more clearly the U.S. government’s willingness and ability to mount a strong defense against the potential enemy. Alternatively, the earlier expenditure on B might cause the enemy to accelerate his own production of weapons or mobilization of troops. These are the kinds of crucial issues that discounting is powerless to illuminate, and may even obscure.

- For a decision to rest on the use of a particular discount rate, there must be great certainty about the future costs and effectiveness of the alternatives. But there seldom is. The practice of discounting therefore promotes an illusion of certainty — a potentially dangerous illusion, in the case of national defense.

- Finally, the “correct” discount rate depends on the options available to a particular manager of a particular government activity. Yet Thaler insists on the application of a uniform discount rate by all government managers (p. 6). By Thaler’s own example, such a practice could lead a manager to choose the wrong option.

So even if there is certainty about everything else, there is no “correct” discount rate, and it is presumptuous of Thaler to prescribe one on the assumption that it will fit every defense manager’s particular circumstances.**

Thaler does the same thing when he counsels intervention in personal decisions because too many people — in his view — make irrational decisions.

In the context of personal decision-making — which is the focal point of Thaler’s “libertarian” paternalism — the act of discounting is rational because it serves wealth-maximization. But life isn’t just about maximizing wealth. That’s why some people choose to have a lot of children, when doing so obviously reduces the amount that they can save. That’s why some choose to retire early rather than stay in stressful jobs. Rationality and wealth maximization are two very different things, but a lot of laypersons and too many economists are guilty of equating them.

If wealth-maximization is your goal, just stop drinking, smoking, enjoying good food, paying for entertainment, subscribing to newspapers and magazines, buying books, watering your lawn, mowing the grass, driving your car (except to work if you have no feasible alternative), and on into the night. You will accumulate a lot of money — if you invest wisely (there’s the rub of uncertainty) — but you will live a miserable life, unless you are the rare person who is a true miser.

__________

* If you are unfamiliar with the background of the Clark-Thaler exchange, and the reference to fiscal constraints, here’s the story: Since 1969 the Secretary of Defense has required the military departments to propose multi-year spending programs that are constrained by an explicit ceiling on each year’s spending. Fiscal guidance, as it is called, was lacking before that. But, in reality, defense budgets have always been constrained, ultimately by Congress. Fiscal guidance represents only a rough guess as to the total amount of defense spending that Congress will approve, and a rougher guess about the distribution of that spending among the military departments.

** Thaler’s example of a cost-saving investment is also a stretch, given how government budgets are decided. I gave it a pass in order to make the point that it wouldn’t save Thaler’s argument even if it were realistic. Here’s the missing reality:

Even if the Secretary of Defense (the grand panjandrum of defense managers) makes the kinds of moves counseled by Thaler, and even if his multi-year program sails through the Office and Management and Budget without a scratch, Congress has the final say. And Congress, though it pays attention to the multi-year plans coming from the Executive Branch, still makes annual appropriations. When it does so, it essentially ignores the internal logic of the multi-year plans (assuming that the Defense plan has an internal logic after it has been subjected to Pentagon politics). Instead, Congress divides the defense budget into various spending programs (see the list for national defense, here), and adjusts each program to suit the tastes, preferences, and moods of staffers, committee members, and committee chairman. Thus it is unlikely that the services’ maintenance and procurement budgets will emerge from Congress as they entered, with cross-temporal tradeoffs intact. A more rational budgeting strategy, from the perspective of the Secretary of Defense, is to submit plans that accord with the known preferences of Congress. Such plans may not incorporate the kind of trivial fine-tuning favored by Thaler, but they will more likely serve the national interest by yielding a robust defense.