This post is an adaptation of an article that I wrote 25 years ago. It appeared in the May-June 1989 issue of Program Manager, a magazine published in 1972-2003 by the Defense Systems Management College and its successor, the Defense Acquisition University. Several years before the article appeared, I had begun to question the soundness of the federal government’s official policy about discounting. which is stated in Circular A-94, issued by the Office of Management and Budget, Executive Office of the President.

The point of this post is to refute the case for discounting in benefit-cost or cost-effectiveness analyses of government projects. Part of my argument against discounting is made in “Discounting and ‘Libertarian Paternalism’.” This post makes a more complete case against the use of discounting in analyses of government projects.

DISCOUNTING: WHY AND WHY NOT

Discounting is a valid exercise in the evaluation of personal and business alternatives. A business, for example, will use discounting to compare alternative investments in new equipment; for example:

Implementation of project A will cost $1 million a year in years 1-5; project A will yield an annual net cash flow of $1 million in years 6-15.

Implementation of B will cost $1.5 million a year in years 1-4; B will yield $1.1 million a year in years 5-15.

Instead of undertaking either project, the firm could purchase equally risky bonds with a yield of 5 percent.

Should the firm undertake project A or project B? Discounting reveals the answer (though, for the sake of simplicity, I’m omitting risk, uncertainty, taxes, and inflation): The net present value of A, discounted at 5 percent, is $1.72 million; of B, $4.34 million. B is the preferred alternative, all other things being equal.

This result would seem backwards to a person who is used to thinking in terms of gross numbers, irrespective of the timing of outlays and returns. For example, A costs $5 million and returns $1 million a year (20 percent) when it’s up and running; whereas, B costs $6 million and returns $1.1 million a year (18.33 percent) when it’s up and running. Thus an analysis that omits timing would favor project A. But timing is important. Even though B costs more than A, B yields a greater return, and sooner (by a year). Over the relevant time span, the extra year and extra annual return of $0.1 million make B the more profitable alternative.

However, the result is sensitive to the selection of a discount rate and time horizon, both of which are judgment calls. A range of discount rates and time horizons would be chosen, to see if the preference for B is robust or weak. If A is judged less risky than B, it would be appropriate to apply a lower discount rate to A than to B. If A is likely to have a longer productive life than B (less likely to become obsolete, for example), the time horizon for A would be longer than for B.

Discounting makes sense in the private sector, despite the sensitivity of results to changes in assumptions about costs, returns, discount rate, and time horizon. For one thing, the discount rate — however uncertain — is relevant to the decision-maker; it represents the rate of return that the decision-maker could earn if he chose not to undertake project A or project B. It is his discount rate, not one chosen arbitrarily for him by someone else. For another thing, the returns (such as they turn out to be) belong to the decision-maker. When all is said and done, he (or the principal for whom he is acting) will choose a course of action that is meant to maximize his wealth or his profits. Accordingly, different decision-makers, in different circumstances, will use discount rates and time horizons appropriate to their circumstances. Discounting isn’t a one-size-fits-all procedure.

That said, it doesn’t make sense if to discount if you’re analyzing alternative projects for a government decision-maker. Why not?

1. Government is funded (ultimately) by taxes. Taxpayers have myriad discount rates. The use of a particular rate to represent a (fictional) “social” rate amounts to gross presumption.

2. Further, there’s usually a misalignment of costs and benefits. Those who bear the costs (taxpayers) aren’t likely to reap the benefits in proportion to the costs they bear. Discounting doesn’t apply when X bears the costs and Y reaps the benefits.

3. Given (1) and (2), the proponent of discounting will resort to the use of an internal rate of return (e.g., cost reductions generated by maintenance projects that can then be applied to investments in new weapon systems). The use of an internal rate of return turns out to be a horse-before-the cart proposition: the correct choice determines the discount rate; the discount rate doesn’t determine the correct choice.

Now, for the details.

THE FICTIONAL “SOCIAL” DISCOUNT RATE

The academic justification for discounting the costs of alternative government projects goes like this:

The appropriate rate of discount for public projects is one which measures the social opportunity cost. The decision to devote resources to investment in a public project means … that these resources will become unavailable for use by the private sector. And this transfer should be undertaken whenever a potential project available to the government offers social benefits greater than the loss sustained by removing these resources from the private sector. The social rate of discount, then, must be chosen in such a way that it leads to a positive number for the evaluated net benefits of a public project if and only if its gross benefits exceed its opportunity costs in the private sector. (William J. Baumol, “On the Social Rate of Discount,” American Economic Review, September 1968, pp. 789-90)

In mathematical notation:

[NPV(public benefits) > NPV(private costs)] → Undertake public project

In the next section I’ll address the almost-certain misalignment of benefits and costs. Here, I’ll assume for the sake of argument that benefits flow only to those taxpayers who foot the bill for a public (i.e., government) project, and do so in perfect proportion to the taxes levied on each of them. Would that unlikely condition justify the public project?

Consider this example:

There is a two-person economy consisting of Adam and Eve.

If a public project is undertaken, both will be taxed the same amount and both will receive the same benefits.

Taxes are levied in year 1; benefits are received in year 2.

Adam’s discount rate is 5 percent; Eve’s discount rate is 10 percent. That is, Eve has a “high” time-preference, relative to Adam; she places more emphasis on the present, as against the future.

The public decision-maker uses a discount rate of 7.5 percent.

The dollar value of the benefits accruing to Adam and Eve can be estimated.

The net present value of the sum of those benefits exceeds the net present value of the sum of the costs borne by Adam and Eve.

Nevertheless, Eve is probably made worse off by the undertaking of the public project. Adam is probably made better off, but at Eve’s expense. Why? Let’s say that Adam and Eve each pay $100 in taxes in year 1, and that the public project breaks even (returns exactly 7.5 percent), so that each of them receives $107.50 worth of benefits in year 2. Adam, given his 5 percent discount rate, would have been made whole with benefits of $105 in year 2, so he gains $2.50. Eve, on the other hand, would have been made whole with benefits of $110 in year 2, so she loses $2.50.

All of that assumes, of course, that both Adam and Eve place any value on the benefits delivered by the public project, let alone the same value. How does the government decision-maker know what value Adam and Eve place on the benefits delivered by his project? He doesn’t; he’s just a presumptuous fellow who wants to spend Adam and Eve’s money to satisfy his own sense of how things should be.

THE MISALIGNMENT OF COSTS AND BENEFITS

Professor Baumol admits that “no optimal [social discount] rate exists” (op. cit., p. 798). Actually, no “social” discount rate exists, except in the minds of arrogant economists and government officials.

How does “society” benefit if Adam is made happy at Eve’s expense? It doesn’t, because there’s no such thing as a social-welfare function, that is, a collective degree of happiness (or unhappiness) in which Adam’s gain somehow cancels Eve’s loss.

It only gets worse in the usual case, where the benefits from a government program do not flow to taxpayers in proportion to the taxes that they pay. It would be a major miracle if benefits were somehow aligned perfectly or even passably well with tax payments, especially given progressive tax rates and deliberately regressive benefit payments (e.g., Social Security, Medicare, Medicaid, housing subsidies, food stamps).

With millions of taxpayers and non-taxpayers in the mix — each with his own discount rate, and each receiving benefits (or not) that are disproportionate to the taxes that he pays — how can anyone say with a straight face that any government project can be justified by applying a “social” discount rate to its benefits and costs?

THE IRRELEVANT INTERNAL RATE OF RETURN

Given the foregoing, insurmountable objections, the die-hard defender of public-sector discounting hops on his deus ex machina: the internal rate of return. One such die-hard is Richard Thaler (also a notorious paternalist and purported libertarian), who essayed his views in “Discounting and Fiscal Constraints: Why Discounting is Always Right” (Center for Naval Analyses, Professional Paper 257, August 1979).

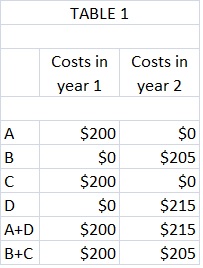

In Thaler’s simplified version of reality, a government decision-maker (manager) faces a choice between two projects that would deliver equal effectiveness (benefits). Specifically, the manager must choose between project A, at a cost of $200 in year 1, and equally-effective project B, at a cost of $205 in year 2 (op. cit., pp. 1-2). Thaler continues:

A [government] manager . . . cannot earn bank interest on funds withheld for a year. . . . However, there will generally exist other ways for the manager to “invest” funds which are available. Examples include cost-saving expenditures, conservation measures, and preventive maintenance. These kinds of expenditures, if they have positive rates of return, permit a manager to invest money just as if he were putting the money in a savings account.

. . . Suppose a thorough analysis of cost-saving alternatives reveals that [in year 2] a maintenance project will be required at a cost of $215. Call this project D. Alternatively the project can be done [in year 1] (at the same level of effectiveness) for only $200. Call this project C. All of the options are displayed in table 1.

(op. cit., pp. 3-4)

Thaler believes that his example clinches the argument for discounting because the choice of project B (an expenditure of $205 in year 2) enables the manager to undertake project C in year 1, and thereby to “save” $10 in year 2.

Thaler’s “proof” is deeply flawed, as discussed in “Discounting and ‘Libertarian Paternalism’.” I’ll focus here on the essential emptiness of Thaler’s argument:

1. Even granting the availability of cost-reduction measures, their payoffs will vary widely. Thaler conveniently conjures projects C and D, with costs of $200 and $215 in years 1 and 2, respectively. He could just have well conjured a project D with a cost of $205 in year 2 — throwing A + D into a tie with B + C — or a project D with a cost of $203 in year 2 — causing A + D to look better than B + C.

2. In other words, the “correct” discount rate depends on the options available to a specific manager of a specific government activity. Yet Thaler insists on the application of a uniform discount rate by all government managers (op. cit., p. 6). By Thaler’s own example, such a practice could lead a manager to choose the wrong option.

3. To put it another way, the analyst should consider the specific options that are available to a specific manager, by constructing packages of projects that would cost the about the same in every year. Having done so (and assuming away a great deal of uncertainty about the costs and benefits of the options), the manager can then choose the package that delivers the most bang for the buck — when the bang is needed, in his judgment. There is no need to apply a discount rate. The relevant (and idiosyncratic) “discount rate” is a product of the correct choice, not a determinant of it.

FINAL WORDS ABOUT THE FUTILITY OF DISCOUNTING FOR GOVERNMENT DECISION-MAKING

Even if there were such a thing as a “social” discount rate, and even if the costs and benefits of government programs were well aligned, discounting would be an inadvisable practice in analysis for government decision-making. If a decision is to depend on the application of a particular discount rate, there must be great certainty about the future costs and benefits of alternative courses of action. But there seldom is (see “Analysis for Government Decision-Making: Demi-Science, Hemi-Demi-Science, and Sophistry“). The practice of discounting simply fosters an illusion of certainty — a potentially dangerous illusion, in the case of national defense.