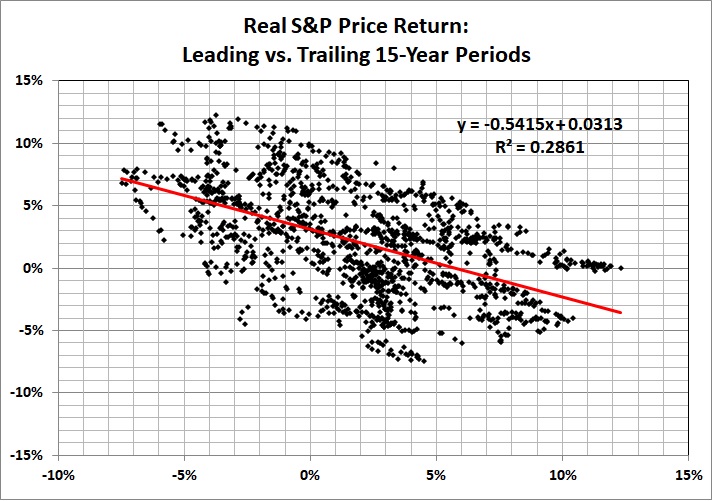

It’s everywhere, but most notably in the stock market and in election returns.

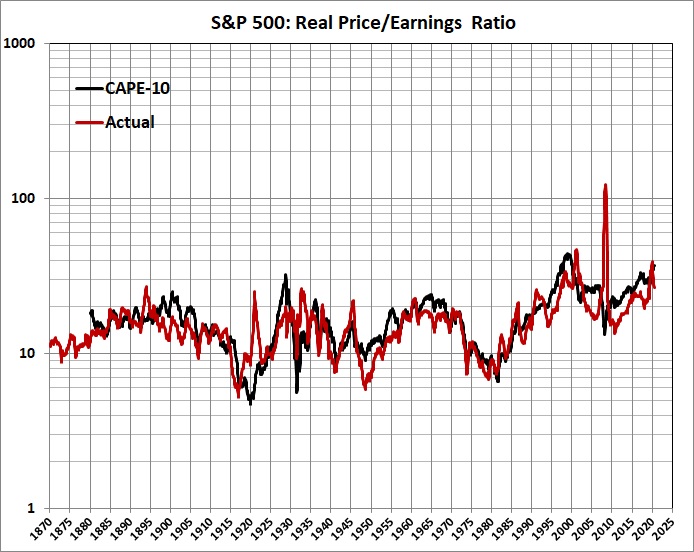

In the stock market, as exemplified by the S&P 500 index, there have been wild swings in the price-earnings ratio:

Derived from Robert Shiller’s data set. CAPE-10 is the cyclically adjusted price/earnings ratio, where the cyclical adjustment amounts to a 10 year average of the ratio.

In a world where stock buyers weren’t driven by irrational exuberance — and irrational pessimism — the PE ratio would follow something like a straight line. It might be a rising straight line because, as some analysts have noted, stock buyers have acquired an increasingly greater tolerance for risk-taking. But it would be close to a straight line.

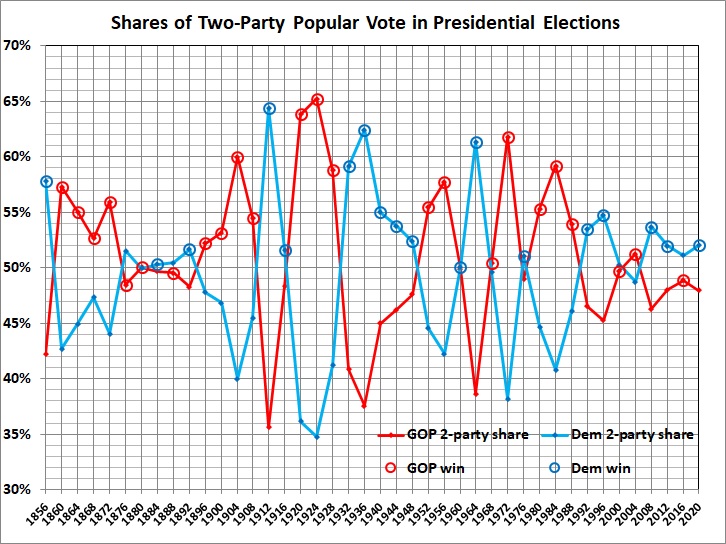

The zigs and zags of the stock market are echoed in the outcomes of presidential elections:

Derived from Dave Leip’s Atlas of U.S. Presidential Elections.

To put it bluntly, almost every American who values his liberty and prosperity would in most elections have preferred the Republican candidate as the lesser of two evils. The success of Democrats testifies to the gullibility of many voters, who are swayed by — among other things — asymmetrical ideological warfare:

Leftists have the advantage of saying the kinds of things that people like to hear, especially when it comes to promising “free” stuff and visions of social perfection….

[L]eftists have another advantage: they’re ruthless. Unlike true conservatives (not Trumpsters) and most libertarians, leftists can be ruthless, unto vicious. They pull no punches; they call people names; they skirt the law — and violate it — to get what they want (e.g., Obama’s various “executive actions”); they use the law and the media to go after their ideological opponents; and on and on.

Why the difference between leftists and true conservatives? Leftists want to rearrange the world to fit their idea of perfection. They have it all figured out, and dissent from the master plan will not be tolerated. (This is very Hitleresque and Stalinesque.) Conservatives and libertarians want people to figure out for themselves how to arrange the world within the roomy confines of simple morality (don’t cheat, don’t steal, don’t murder, etc.).

The left’s ruthlessness was in full spate last year, when the election was bought and probably stolen as well.

In the same post (published on July 23, 2016), my prescience was on display:

If Trump wins in November — a very big “if” — it should be an object lesson to true conservatives and libertarians. Take the gloves off and don brass knuckles. This isn’t a contest for hockey’s Lady Byng Trophy. To change the sports metaphor, we’re in the late rounds of a brutal fight, and well behind on points. It’s time to go for the knockout.

The good news is that recent elections reflect the effects of political polarization. The swings have become less pronounced because the electorate’s “squishy center” has shrunk. The challenge before the GOP is to convince what remains of the “squishy center” that it is in their best interest to reject the anti-libertarian and anti-prosperity policies of the Democrat Party, which has become nothing more than a mouthpiece for an (anti) American brand of Hitlerism and Stalinism.