A REISSUE (WITHOUT UPDATES) OF THE ORIGINAL POST DATED DECEMBER 7, 2011

Interest rates reflect the supply of and demand for funds. Money is tighter now than it was in the years immediately before the onset of the Great Recession. Tim Congdon explains:

In the three years to October 2008, the quantity of money soared from $10,032 billion to $14,186 billion, with a compound annual growth rate of just over 12 per cent. The money growth rate in this period was the highest since the early 1970s. Indeed, 1972 and 1973 had many similarities to 2006 and 2007, with bubbling asset markets, buoyant consumer spending and incipient inflationary pressures. On the other hand, in the three years from October 2008 the quantity of money was virtually unchanged. (It stood at $14,340 billion in October 2011.) In other words, in the three years of the Great Recession the quantity of money did not increase at all.

But if money is relatively tight, why are interest rates so low? For example, as of October 2011, year-over-year inflation stood at 3.53 percent (derived from CPI-U estimates, available here). In October, Aaa bond yields averaged 3.98 percent, for a real rate of about 0.4 percent; Baa bond yields averaged 5.37 percent, for a real rate of about 1.8 percent; and conventional mortgages averaged 4.07 percent, for a real rate of about 0.5 percent. By contrast, in 1990-2000, when the CPI-U rose at an annual rate of 3.4 percent, real Aaa, Baa, and conventional mortgage rates hovered in the 4-6 percent range. (Real rates are derived from interest rate statistics available here.)

The reason for these (and other) low rates is that borrowers have become less keen about borrowing; that is, they lack confidence about future prospects for income (in the case of households) and returns on investment (in the case of businesses). Why should that be?

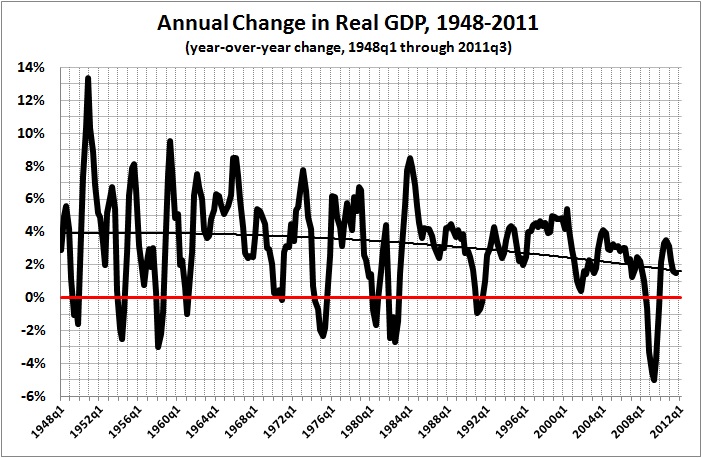

If the post-World War II trend is any indication — and I believe that it is — the American economy is sinking into stagnation. Here is the long view:

- 1790-1861 — annual growth of 4.1 percent — a booming young economy, probably at its freest

- 1866-1907 — annual growth of 4.3 percent — a robust economy, fueled by (mostly) laissez-faire policies and the concomitant rise of technological innovation and entrepreneurship

- 1908-1929 — annual growth of 2.2 percent — a dispirited economy, shackled by the fruits of “progressivism” (e.g., trust-busting, regulation, the income tax, the Fed) and the government interventions that provoked and prolonged the Great Depression.

- 1947-1969 — annual growth of 3.9 percent — a rejuvenated economy, buoyed by the end of the New Deal, the forced saving that occurred during World War II, and (possibly) the fruits of advances in technology and business operations that were made but not exploited during the Depression (all proof that the rate of growth didn’t decline in the preceding era simply because the economy had “aged”).

- 1970-2010 — annual growth of 2.8 percent – sagging under the cumulative weight of “progressivism,” New Deal legislation, LBJ’s “Great Society” (with its legacy of the ever-expanding and oppressive welfare/transfer-payment schemes: Medicare, Medicaid, a more generous package of Social Security benefits), and an ever-growing mountain of regulatory restrictions.

(From this post, as updated in this one.)

And here is the post-World War II view:

This trend cannot be reversed by infusions of “stimulus spending” or “quantitative easing.” It reflects an underlying problem that cannot be cured by those simplistic macroeconomic “fixes.”

The underlying problem is not “tight money,” it is that American businesses are rightly pessimistic about an economic future that is dominated by a mountain of debt (in the form of promised “entitlements”) and by an ever-growing regulatory burden. Thus business investment has been a decline fraction of private-sector GDP:

Derived from Bureau of Economic Analysis, Table 1.1.5. Gross Domestic Product (available here). The numerator is gross private domestic investment (GPDI, line 7) less the residential portion (line 12). The denominator is GDP (line 1) less government consumption expenditures and gross investment (line 21).

As long as business remains (rightly) pessimistic about the twin burdens of debt and regulation, the economy will sink deeper into stagnation. The only way to overcome that pessimism is to scale back “entitlements” and regulations, and to do so promptly and drastically.

In sum, the present focus on — and debate about — conventional macroeconomic “fixes” (fiscal vs. monetary policy) is entirely misguided. Today’s economists and policy-makers should consult Hayek, not Keynes or Friedman or their intellectual descendants. If economists and policy-makers would would read and heed Hayek — the Hayek of 1944 onward, in particular — they would understand that our present and future economic morass is entirely political in origin: Failed government policies have led to more failed government policies, which have shackled both the economy and the people.

Economic and political freedoms are indivisible. It will take the repeal of the regulatory-welfare state to restore prosperity and liberty to the land.