UPDATED 04/19/15 WITH THE ADDITION OF TWO ENTRIES

Links to the other posts in this occasional series may be found at “Favorite Posts,” just below the list of topics.

* * *

Paul Mirengoff explores the similarities between Neville Chamberlain and Barack Obama; for example:

We see with Chamberlain the same curious dynamic present in the Obama presidency. At home, a tough-as-nails administration/political machine that takes no prisoners and rarely compromises; abroad, a feckless operation with a pattern of caving to belligerent adversaries. [“Neville Chamberlain and Barack Obama: The Similarities Run Deep,” Powerline Blog, April 15, 2014]

See also John Hinderaker’s Powerline post, “Daniel Pipes: The Obama Doctrine Serves Up One Disaster After Another” (April 6, 2015), and a piece by Eileen F. Toplansky,”Obama’s Three Premises” (American Thinker, April 20, 2015).

What is Obama up to? For my take, see “Does Obama Love America?”

* * *

If it were possible to convince a climate alarmist that he is wrong, Christopher Monckton of Brenchley is the man for the job:

“What Evidence,” asks Ronald Bailey’s headline (www.reason.com, April 3, 2015), “Would Convince You That Man-Made Climate Change Is Real?”

The answer: a rational, scientific case rooted in established theory and data would convince me that manmade climate change is a problem. That it is real is not in doubt, for every creature that breathes out emits CO2 and thus affects the climate.

The true scientific question, then, is not the fatuous question whether “Man-Made Climate Change Is Real” but how much global warming our sins of emission may cause, and whether that warming might be more a bad thing than a good thing.

However, Mr Bailey advances no rational case. What, then, are the elements of a rational, scientific case that our influence on the climate will prove dangerous unless the West completes its current self-shutdown?… [“How to Convince a Climate Skeptic He’s Wrong,” Watts Up With That, April 9, 2015]

There follows a step-by-step dismantling of Mr. Bailey’s case for alarmism. Lord Monckton ends with this:

[I]f Mr Bailey does me the courtesy of reading the above, he will realize that temperatures are not rising by much, glacial ice-melt (if occurring) is on too small a scale to raise sea level by much, global sea ice extent shows little change in two generations, ditto northern-hemisphere snow cover, there has been little increase in rainfall and (according to the IPCC) little evidence for “stronger rainstorms”, and the ocean warming is so small that it falls within the considerable measurement error.

The evidence he adduces is questionable at best on every count. The Temple of Thermageddon will have to do better than that if it wants to convince us in the teeth of the evidence….

…[N]o rational scientific or economic case can be made for taking any action whatsoever today in a probably futile and certainly cost-ineffective attempt to make global warming that is not happening as predicted today go away the day after tomorrow.

The correct policy to address what is likely to prove a non-problem – and what, even if it were every bit as much of a problem as the tax-gobblers would wish, could not by even their most creative quantitative easing be cost-effectively solved by any attempt at mitigation – is to have the courage to do nothing now and adapt later if necessary.

The question is why, in the teeth of the scientific and economic evidence, nearly all of the global governing class were so easily taken in or bought out or both by the strange coalescence of powerful vested interests who have, until now, profited so monstrously by the biggest fraud in history at such crippling expense in lives and treasure to the rest of us, and at such mortal threat to the integrity and trustworthiness of science itself. [Ibid.]

My own modest effort to quell climate alarmism is summarized in “AGW: The Death Knell.”

* * *

Steve Sailer has some fun with the latest bit of experimental hocus-pocus by the intelligence-isn’t-heritable crowd, as interpreted by a reporter for The Washington Post:

In the last few years, there appears to have been a decision to blame racial differences in intelligence on differences in income level, although, of course, that’s not very plausible. That’s what people said way back in 1965, but then the federal Coleman Report of 1966 showed that affluent black students weren’t setting the world on fire academically on average, and vast amounts of data have accumulated validating the Coleman Report ever since.

But a half century later we’re back to asserting the same untested theories as in 1965….

Allow me to point out that a national newspaper has asked a couple of guys who know what they are talking about to punch holes in the latest bit of goodthink and, as of press time, the American public hasn’t dug up Hitler’s DNA and elected it President. So maybe we’re actually mature enough to discuss reality rather than lie all the time?…

Six decades from now, the Education Secretary of the hereditary Bush-Clinton Administration will be declaring the key periods for federal intervention are the eight months and 29 days before birth … but not a day sooner! [“Charles Murray and James Thompson Asked Their Opinions in ‘Post’ Article on Brain Size; World Hasn’t Ended, Yet,” The Unz Review, April 15, 2015]

Along the way, Sailer links to Dr. James Thompson’s post about the article in question. There’s a followup post by Thompson, and this one is good, too. See also this post by Sailer.

Gregory Cochran has a related post (“Scanners Live in Vain,” West Hunter, March 31, 2015), where he says this about the paper and the reporting about it:

There is a new paper out in Nature Neuroscience, mainly by Kimberly Noble, on socioeconomic variables and and brain structure: Family income, parental education and brain structure in children and adolescents. They found that cortex area went up with income, although more slowly at high incomes. Judging from their comments to the press, the authors think that being poor shrinks your brain.

Of course, since intelligence is highly heritable, and since people in higher social classes, or with high income, have higher average IQs (although not nearly as high as I would like), you would expect their kids to be, on average, smarter than kids from low-income groups (and have larger brains, since brain size is correlated with IQ) for genetic reasons. But I guess the authors of this paper have never heard of any of that – which raises the question, did they scan the brains of the authors? Because that would have been interesting. You can actually do microscopic MRI.

Even better, in talking to Nature, another researcher, Martha Farah, mentions unpublished work that shows that the brain-size correlation with SES is already there (in African-American kids) by age one month!

Of course, finding that the pattern already exists at the age of one month seriously weakens any idea that being poor shrinks the brain: most of the environmental effects you would consider haven’t even come into play in the first four weeks, when babies drink milk, sleep, and poop. Genetics affecting both parents and their children would make more sense, if the pattern shows up so early (and I’ll bet money that, if real, it shows up well before one month); but Martha Farah, and the reporter from Nature, Sara Reardon, ARE TOO FUCKING DUMB to realize this.

And John Ray points to this:

Quick thinkers are born not made, claim scientists.

They have discovered a link between our genes and the ability to remain mentally on the ball in later life.

It is the first time a genetic link has been shown to explain why some people have quick thinking skills.

Researchers identified a common genetic variant – changes in a person’s genetic code – related to how quickly a person is able to process new information. [Jenny Hope, “Quick Thinkers Are Born Not Made: The Speed at Which We Process New Information Is Written in Our Genes,” DailyMail.com, April 16, 2015]

Dr. Ray links to the underlying studies, here.

I’ve probably said more than I should say about the heritability of intelligence in “Race and Reason: The Achievement Gap — Causes and Implications,” “Evolution and Race,” “‘Wading’ into Race, Culture, and IQ,” and “The Harmful Myth of Inherent Equality.”

* * *

Speaking of equality, or the lack thereof, Daniel Bier explains “How Piketty Manufactured Rising [Wealth] Inequality in 6 Steps” (Foundation for Economic Education, April 9, 2015):

Piketty’s chart on US wealth inequality displayed a trend that none of its original sources showed. Worst of all, he didn’t tell his readers that he had done any of this, much less explained his reasoning.

But now Magness has deconstructed the chart and shown, step by step, how Piketty tortured his sources into giving him the result he wanted to see….

If your methods can produce opposite results using the same sources, depending entirely on your subjective judgment, you’re not doing science — you’re doing a Choose Your Own Adventure story where you start from the conclusion and work backwards.

Now that you’ve seen how it’s done, you too can “piketty” your data and massage your narrative into selling 1.5 million books — that almost no one will actually read, but will be widely cited as justification for higher taxes nonetheless.

Committed leftists will ignore Piketty’s step back from extreme redistributionism, which I discussed in “Not-So-Random Thoughts (XIII).”

* * *

Committed leftists will lament the predicate of “Has Obamacare Turned Voters Against Sharing the Wealth?” (The New York Times, April 15, 2015). The author of the piece, Thomas B. Edsall (formerly of The Washington Post), clearly laments the possibility. (I do not, of course.) Edsall’s article is full of good news (for me); for example:

In 2006, by a margin of more than two to one, 69-28, those surveyed by Gallup said that the federal government should guarantee health care coverage for all citizens of the United States. By late 2014, however, Gallup found that this percentage had fallen 24 points to 45 percent, while the percentage of respondents who said health care is not a federal responsibility nearly doubled to 52 percent.

Edsall’s main worry seems to be how such a mood shift will help Republicans. Evidently, he doesn’t care about taxpayers, people who earn their income, or economic growth, which is inhibited by redistribution from “rich” to “poor.” But what else is new? Edsall is just another representative of the elite punditariat — a member of the “top” part of the left’s “top and bottom” coalition.

Edsall and his ilk should be worried. See, for example, “The Obamacare Effect: Greater Distrust of Government” (the title tells the tale) and “‘Blue Wall’ Hype” which debunks the idea that Democrats have a lock on the presidency.

* * *

The question of nature vs. nurture, which I touched on three entries earlier, is closely related to the question of innate ability vs. effort as the key to success in a field of endeavor. “Scott Alexander” of Slate Star Codex has written at length about innate ability vs. effort in two recent posts: “No Clarity Around Growth Mindset…Yet” and “I Will Never Have the Ability to Clearly Explain My Beliefs about Growth Mindset.” (That should be “to explain clearly.”)

This is from the first-linked post:

If you’re not familiar with it, growth mindset is the belief that people who believe ability doesn’t matter and only effort determines success are more resilient, skillful, hard-working, perseverant in the face of failure, and better-in-a-bunch-of-other-ways than people who emphasize the importance of ability. Therefore, we can make everyone better off by telling them ability doesn’t matter and only hard work does.

This is all twaddle, as “Alexander” shows, more or less, in his two very long posts. My essay on the subject is a lot shorter and easier to grasp: “The Harmful Myth of Inherent Equality.”

* * *

ENTRIES ADDED 04/19/15:

Obamacare, not unsurprisingly to me, has led to the rationing of health care, according to Bob Unruh’s “Obamacare Blocks Patients Paying for Treatment” (WND, March 6, 2014). And Aleyne Singer delivers “More Proof Obamacare Is Increasing Coverage but Not Access to Health Care” (The Daily Signal, December 9, 2014).

None of this should surprise anyone who thought about the economics of Obamacare, as I did in “Rationing and Health Care,” “The Perils of Nannyism: The Case of Obamacare,” “More about the Perils of Obamacare,” and “Health-Care Reform: The Short of It.”

* * *

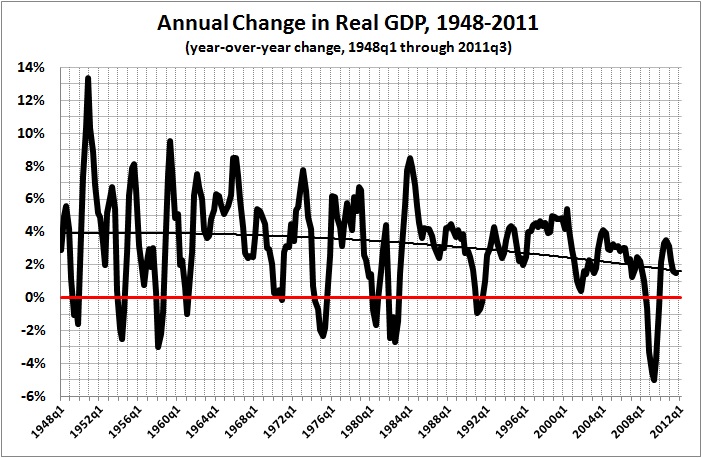

Ben Bernanke asks “Why Are Interest Rates So Low?” (Ben Bernanke’s Blog, March 30, 2015). His answer? In so many words, business is bad, which means that the demand for capital financing is relatively weak. But in a followup post, “Why Are Interest Rates So Low, Part 2: Secular Stagnation” (Ben Bernanke’s Blog, March 31, 2015), Bernanke argues that the problem isn’t secular stagnation.

I agree that interest rates are low because the economy remains weak, despite some recovery from the nadir of the Great Recession. But, unlike Bernanke, I don’t expect the economy to make a full recovery — and I’m talking about real growth, not phony unemployment-rate recovery. Why Not? See “Obamanomics in Action” and “The Rahn Curve Revisited.” The economy will never grow to its potential as long as the dead hand of government continues to press down on it.

{kind=link}