I have just come across two articles about the shrinking number of firms listed on U.S. stock exchanges:

Kathleen Kahle and René M. Stulz, “Is the American Public Corporation in Trouble?”, Journal of Economic Perspectives, Volume 31, Number 3, Summer 2017

Michael J. Mauboussin, Dan Callahan, and Darius Majd, “The Incredible Shrinking Universe of Stocks: The Causes and Consequences of Fewer U.S. Equities“, Credit Suisse, Global Financial Strategies, March 22, 2017

I will refer to the first article as K&S and the second article as MC&M. (Despite the publication dates, K&S predates MC&M.) The articles tell this tale:

- From the mid-1970s to the mid-1990s, the number of listed companies rose sharply.

- Since the min-1990s, the number of listed companies has dropped sharply.

- The declining number of listed companies has been accompanied by consolidation within many industries and — among the surviving firms — greater size, higher profits, bigger payouts to shareholders, and higher average market capitalization (market value of outstanding shares).

Here are some relevant observations from K&S:

If consolidation has nothing to do with being a public firm, we should see the total number of firms decreasing, whether firms are public or private. We don’t. The United States has become an economy dominated by service industries, and so a good way to demonstrate this is to look at the service industries. Even though the number of firms in the service industries increases by 30 percent from 1995 to 2014 and employment increases by 240 percent, the number of public firms falls by 38 percent. A similar evolution occurs in the finance industry, in which the number of firms increases by 18.7 percent from 1995 to 2014, but over the same time the number of listed firms falls by 42.3 percent. Further, … the propensity of firms to be listed … falls across all firm-size categories when size is measured by employment….

The drop in the propensity to be listed suggests that there is a problem with being a public firm…. In the United States, corporate law is governed by state of incorporation, but public firms are subject to federal securities laws. As a result, Congress can regulate public firms in ways that it cannot regulate private firms….

Our data show that the fraction of small public firms has dropped dramatically…. [T]he drop in initial public offerings is particularly acute among small firms. Why are public markets no longer welcoming for small firms?… [R]esearch and development investments have become more important. Generally, R&D is financed with some form of equity rather than debt, at least in early stages before a firm has accumulated lucrative patents. Raising equity in public markets to fund R&D can be difficult. Investors want to know what they invest in, but the more a firm discloses, the more it becomes at risk of providing ammunition to its competitors. As a result, R&D-intensive firms may be better off raising equity privately from investors who then have large stakes….

There are several additional potential explanations for why small firms are staying out of public markets… First, public markets have become dominated by institutional investors…. Investing in really small firms is unattractive for institutional investors, because they cannot easily invest in a small firm on a scale that works for them. As a result, small firms receive less attention and less support from financial institutions. This makes being public less valuable for these firms. Second, developments in financial intermediation and regulatory changes have made it easier to raise funds as a private firm. Private equity and venture capital firms have grown to provide funding and other services to private firms. The internet has reduced search costs for firms searching for investors. As a result, private firms have come to have relatively easier access to funding.

… According to [the economies of scope] hypothesis, small firms have become less profitable and less able to grow on a stand-alone basis, but are more profitable as part of a larger organization that enables them to scale up quickly and efficiently. Thus, small firms are better off selling themselves to a large organization that can bring a product to market faster and realize economies of scope. This dynamic arises partly because it has become important to get big quickly as technological innovation has accelerated. Globalization also means that firms must be able to access global markets quickly. Further, network and platform effects can make it more advantageous for small firms to take advantage of these effects by being acquired. This hypothesis is consistent with our evidence that the fraction of exchange-listed firms with losses has increased and that average cash flows for smaller firms have dropped…. [M]any mergers do involve small firms, so small firms do indeed choose to be acquired rather than grow as public firms.

The increased concentration we document could also make it harder for small firms to succeed on their own, as large established firms are more entrenched and more dominant….

[Gerald] Davis … argues [in The Vanishing American Corporation] that it has become easier to put a new product on the market without hard assets…. When all the pieces necessary to produce a product can be outsourced and rented, a firm can bring a product to market without large capital requirements. Hence, the firm does not need to go public to raise vast amounts of equity to acquire the fixed assets necessary for production… Ford’s largest production facility in the 1940s, the River Rouge complex, employed more than 100,000 workers at its peak. Of today’s largest US firms, only Amazon has substantially more employees than that complex at its peak. With this evolution, there is no point in going public, except to enable owners to cash out.

These explanations imply that there are fewer public firms both because it has become harder to succeed as a public firm and also because the benefits of being public have fallen. As a result, firms are acquired rather than growing organically. This process results in fewer thriving small public firms that challenge larger firms and eventually succeed in becoming large. A possible downside of this evolution is that larger firms may be able to worry less about competition, can become more set in their ways, and do not have to innovate and invest as much as they would with more youthful competition. Further, small firms are not as ambitious and often choose the path of being acquired rather than succeeding in public markets. With these possible explanations, the developments we document can be costly, leading to less investment, less growth, and less dynamism.

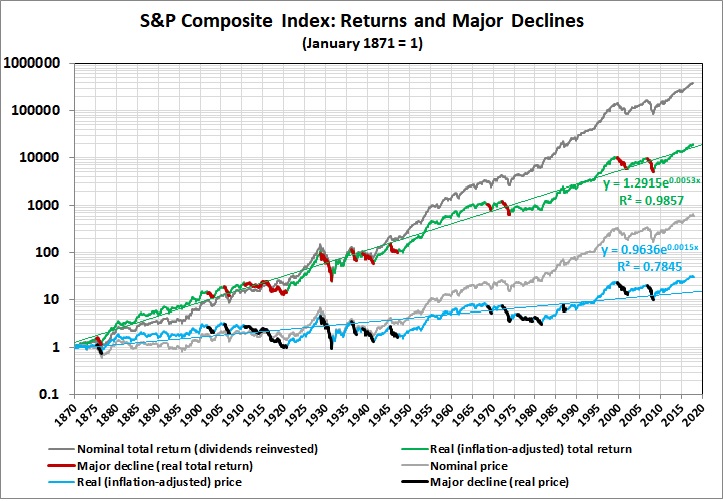

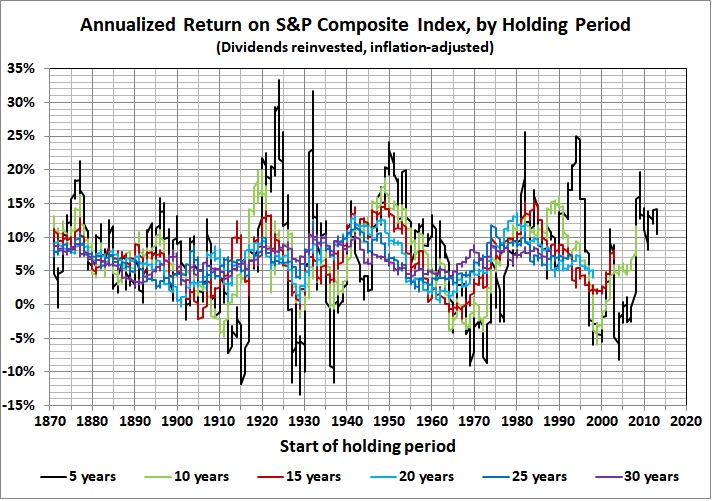

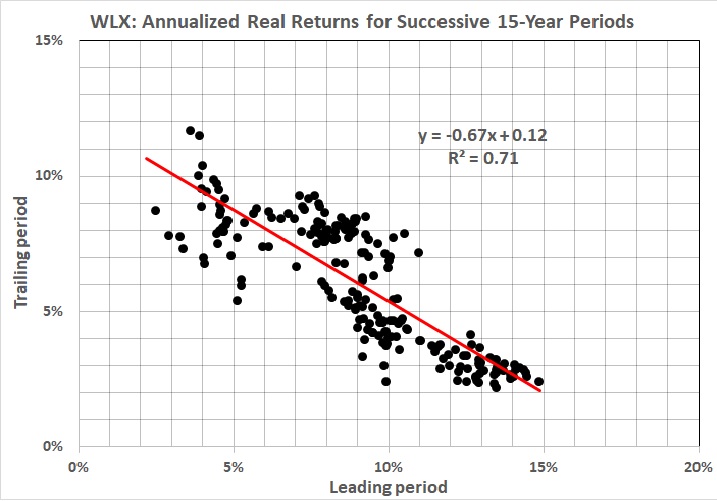

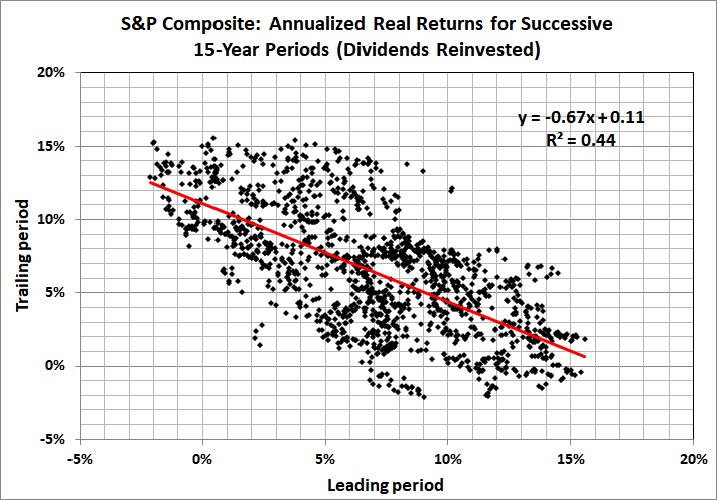

This is all consistent with the creeping stagnation of the U.S. economy, as it collapses under the weight of government spending and regulation: