Robert Higgs asks “How Much Longer Can the U.S. Economy Bear the Burdens?” (The Beacon, a blog of The Independent Institute, January 30, 2015). Higgs explains:

These burdens take the form of taxes, regulations, and uncertainties loaded onto them by governments at every level. Each year, for example, federal departments and regulatory agencies put into effect several thousand new regulations. Only rarely do these agencies remove any existing rules from the Code of Federal Regulations. Thus, the total number in effect continues to climb relentlessly. The tangle of federal red tape becomes ever more difficult for investors, entrepreneurs, and business managers to cut through. Business people have to bear not only a constantly changing, ever more complex array of taxes, fees, and fines, but also a larger and larger amount of regulatory compliance costs, now estimated at more than $1.8 trillion annually. Governments at the state and local levels contribute their full share of such burdens as well.

So it is scarcely a wild-eyed question if we ask, as economist Pierre Lemieux does in a probing article in the current issue of Regulation magazine, whether the U.S. economy is now reacting to these growing burdens by undergoing “a slow-motion collapse.”

The article by Lemieux (“A Slow Motion Collapse” (Regulation, Winter 2014-2015) ends with this:

The resilience of markets, especially in a rich and sometimes still flexible economy like the United States, has dampened the effect of regulation. However, it is reasonable to believe that, over the more than six decades since World War II, regulation has deleted a big chunk of potential prosperity. It has not actually cut into the average standard of living, but this is only a consolation prize, for worse could come if the regulatory bulldozer is not pushed back.

As Higgs suggests, the slow-motion collapse of the economy is due not only to regulation but also to taxation and what Higgs elsewhere calls “regime uncertainty.”

The combined effects of regulation, taxation, and regime uncertainty are captured in the Rahn curve, which depicts the long-term relationship between government spending (as a fraction of GDP) and the rate of economic growth. I say that because government spending and regulatory activity have grown apace since the end of World War II. That might be taken as certainty, of a perverse kind, but beleaguered entrepreneurs can never be certain of the specific obstacles that will be thrown in the path of innovation and investment.

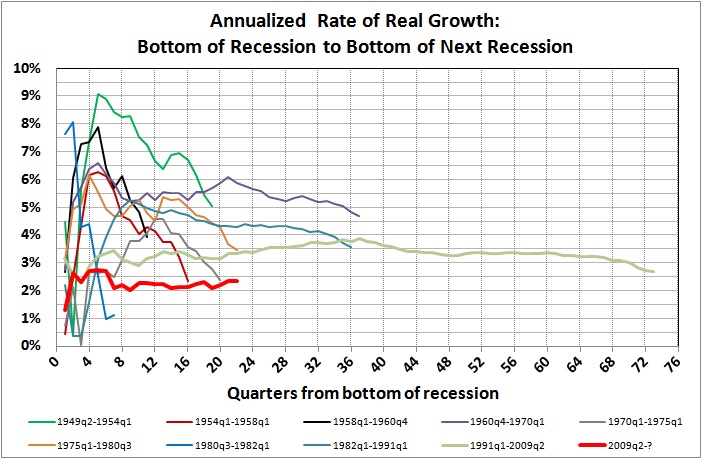

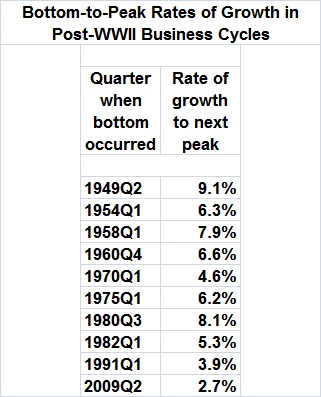

The best evidence of the slow-motion collapse of the U.S. economy is the steady, long-run decline in the rate of economic growth, which is evident in the following graphs:

The graphs are derived from “Current dollar and ‘real’ GDP,” at the website of the Bureau of Economic Analysis of the U.S. Department of Commerce.

As the third graph suggests, the rate of growth has generally declined from business cycle to business cycle.* Thus:

The “Obama recovery” is an anemic thing. Is it any wonder, given Obama’s incessant war on success?

It will take more than a “push back” to restore the economy — and liberty — to health. Obama and his ilk must be driven from office, and kept out of office for good.

* * *

Related posts:

The Laffer Curve, “Fiscal Responsibility,” and Economic Growth

The Causes of Economic Growth

In the Long Run We Are All Poorer

A Short Course in Economics

Addendum to a Short Course in Economics

As Goes Greece

Ricardian Equivalence Reconsidered

The Real Burden of Government

The Illusion of Prosperity and Stability

Taxing the Rich

More about Taxing the Rich

The Keynesian Fallacy and Regime Uncertainty

Why the “Stimulus” Failed to Stimulate

The “Jobs Speech” That Obama Should Have Given

Say’s Law, Government, and Unemployment

Regime Uncertainty and the Great Recession

Regulation as Wishful Thinking

The Commandeered Economy

We Owe It to Ourselves

In Defense of the 1%

Lay My (Regulatory) Burden Down

The Burden of Government

Economic Growth Since World War II

Obama’s Big Lie

Government in Macroeconomic Perspective

Keynesianism: Upside-Down Economics in the Collectivist Cause

Economics: A Survey (also here)

Why Are Interest Rates So Low?

Vulgar Keynesianism and Capitalism

Estimating the Rahn Curve: Or, How Government Spending Inhibits Economic Growth

America’s Financial Crisis Is Now

The Keynesian Multiplier: Phony Math

The True Multiplier

How Libertarians Ought to Thinks about the Constitution

Obamanomics: A Report Card

The Obama Effect: Disguised Unemployment

Income Inequality and Economic Growth

The Rahn Curve Revisited

___________

* Each business cycle runs from the bottom of a recession to the bottom of the next recession. Rather than rely on the National Bureau of Economic Research (NBER), I use my own own definition of a recession, which is:

- two or more consecutive quarters in which real GDP (annualized) is below real GDP (annualized) for an earlier quarter, during which

- the annual (year-over-year) change in real GDP is negative, in at least one quarter.

Unlike the NBER, I do not locate a recession in 2001. Real GDP, measured quarterly, dropped in the first and third quarters of 2001, but each decline lasted only a quarter.

My method of identifying a recession is more objective and consistent than the NBER’s method, which one economist describes as “The NBER will know it when it sees it.” Moreover, unlike the NBER, I would not presume to pinpoint the first and last months of a recession, given the volatility of GDP estimates.