I ended “Shiller’s Folly” with the Danish proverb, it is difficult to make predictions, especially about the future.

Here’s more in that vein. Shiller uses a broad market index, the S&P Composite (S&P), which he has reconstructed back to January 1871. I keep a record of the Wilshire 5000 Full-Cap Total-Return Index (WLX), which dates back to December 1970. When dividends for stocks in the S&P index are reinvested, its performance since December 1970 is almost identical to that of the WLX:

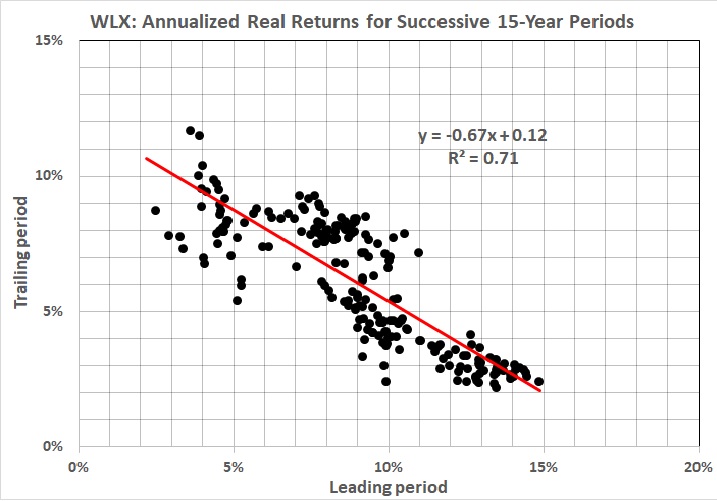

It is a reasonable assumption that if the WLX extended back to January 1871 its track record would nearly match that of the S&P. Therefore, one might assume that past returns on the WLX are a good indicator of future returns. In fact, the relationship between successive 15-year periods is rather strong:

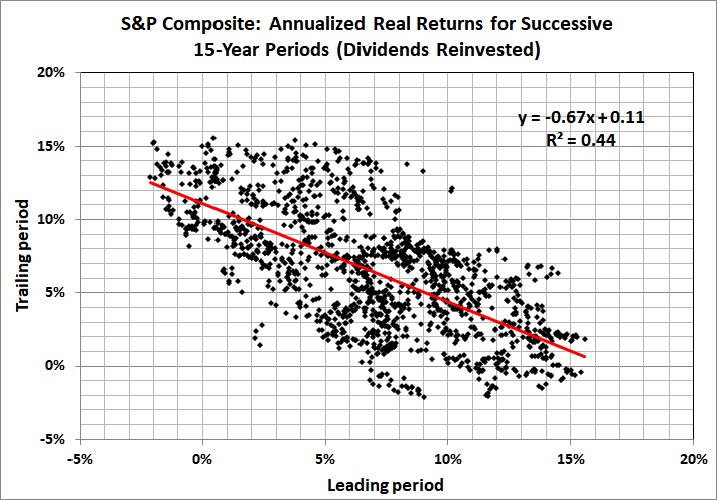

But that seemingly strong relationship is an artifact of the relative brevity of the track record of the WLX. Compare the relationship in the preceding graph with the analogous one for the S&P, which goes back an additional 100 years:

The equations are almost identical — and they predict almost the same real returns for the next 15 years: about 6 percent a year. But the graph immediately above should temper one’s feeling of certainty about the long-run rate of return on a broad market index fund or a well-diversified portfolio of stocks.

Related posts:

Stocks for the Long Run?

Stocks for the Long Run? (Part II)

Bonds for the Long Run?

Much Ado about the Price-Earnings Ratio

Whither the Stock Market?

Shiller’s Folly

A real annual return of 6 percent a year over 15 years isn’t meager, and it will include years with nominal returns of 27 percent or more.

LikeLike

“Results may vary” — and by a lot. That was the point of my post. The past is often a poor basis for predicting the future, especially in the stock market.

LikeLike

You are right about retail investors. And your experience with Contrafund illustrates the virtue of buy-and-hold — it gets you through the rough spots. Your inflation-adjusted, annualized rate of return on Contrafund (as of now) is 6 to 7 percent (6.7, assuming a 35-year holding period). That’s a real, long-run return that most retail investors never remotely approach.

LikeLike

The tricky part is knowing when to cash in because rough spots usually arrive suddenly, and can wipe out years’ worth of gains in a matter of days or weeks.

LikeLike